ABAMEC* Presentation Rio de Janeiro and São Paulo November 2002 * Brazilian Analysts Association.

38

ABAMEC* Presentation Rio de Janeiro and São Paulo November 2002 * Brazilian Analysts Association

-

Upload

stella-daniel -

Category

Documents

-

view

214 -

download

0

Transcript of ABAMEC* Presentation Rio de Janeiro and São Paulo November 2002 * Brazilian Analysts Association.

ABAMEC* Presentation Rio de Janeiro and São Paulo

November 2002

* Brazilian Analysts Association

2

Part I

Corporate Structure

3

CORPORATE STRUCTURE

TELE NORTE LESTE

PARTICIPAÇÕES S.A

79.0% 18.7%

CONTAXCONTAX

TELEMAR PARTICIPAÇÕES

S.A.*

TELEMAR PARTICIPAÇÕES

S.A.*

TELEMARNorte LesteTELEMAR

Norte Leste

Treasury

79.5%

FREE FLOATFREE FLOAT

19.0%

Treasury

*53% of TNE Voting Shares ** Wholly owned subsidiary

FREE FLOATFREE FLOAT

2.3%

1.6%

** **

4

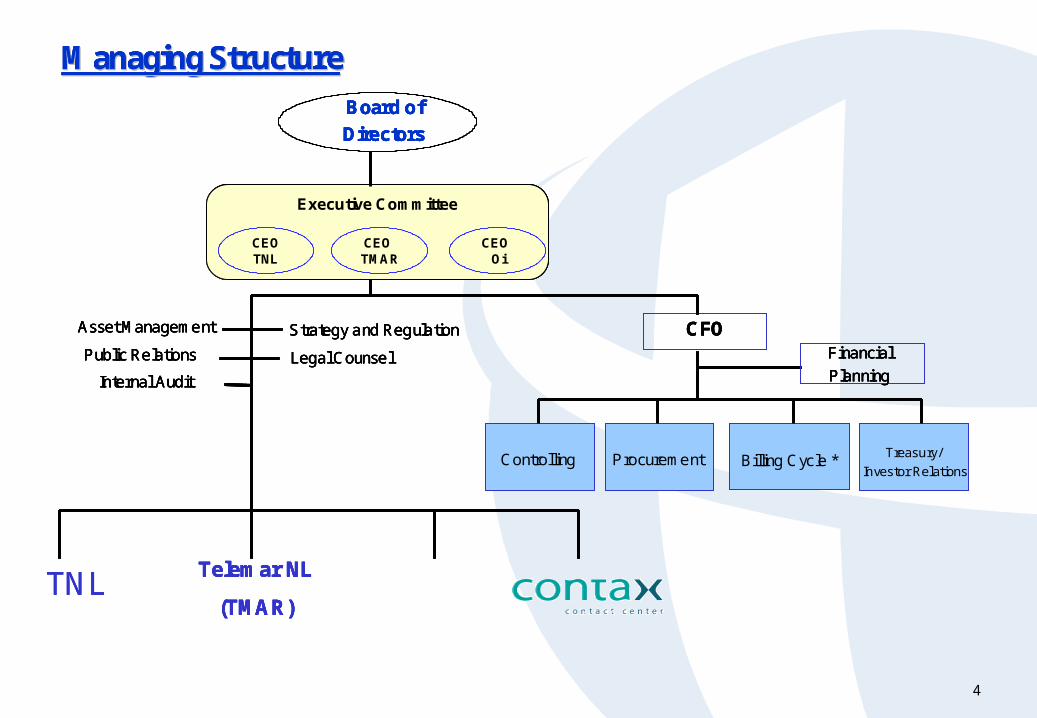

Managing StructureManaging Structure

Board of

Directors

Executive Committee

Controlling Procurement

CFO

Internal Audit

Strategy and Regulation

Legal Counsel Financial

Planning

Asset Management

Public Relations

CEOTNL

CEO TMAR

CEOOi

Billing Cycle *

Telemar NL

(TMAR)

Treasury/

Investor Relations

TNL

Managing StructureManaging Structure

Board of

Directors

Executive Committee

Controlling Procurement

CFO

Internal Audit

Strategy and Regulation

Legal Counsel Financial

Planning

Asset Management

Public Relations

CEOTNL

CEO TMAR

CEOOi

Billing Cycle *

Telemar NL

(TMAR)

Treasury/

Investor Relations

Managing StructureManaging Structure

Board of

Directors

Executive Committee

Controlling Procurement

CFO

Internal Audit

Strategy and Regulation

Legal Counsel Financial

Planning

Asset Management

Public Relations

CEOTNL

CEO TMAR

CEOOi

Billing Cycle *

Telemar NL

(TMAR)

Managing StructureManaging Structure

Board of

Directors

Executive Committee

Controlling Procurement

CFO

Internal Audit

Strategy and Regulation

Legal Counsel Financial

Planning

Asset Management

Public Relations

CEOTNL

CEO TMAR

CEOOi

Billing Cycle *

Telemar NL

(TMAR)

Treasury/

Investor Relations

TNL

5

Part II

TELEMAR NORTE LESTE

6

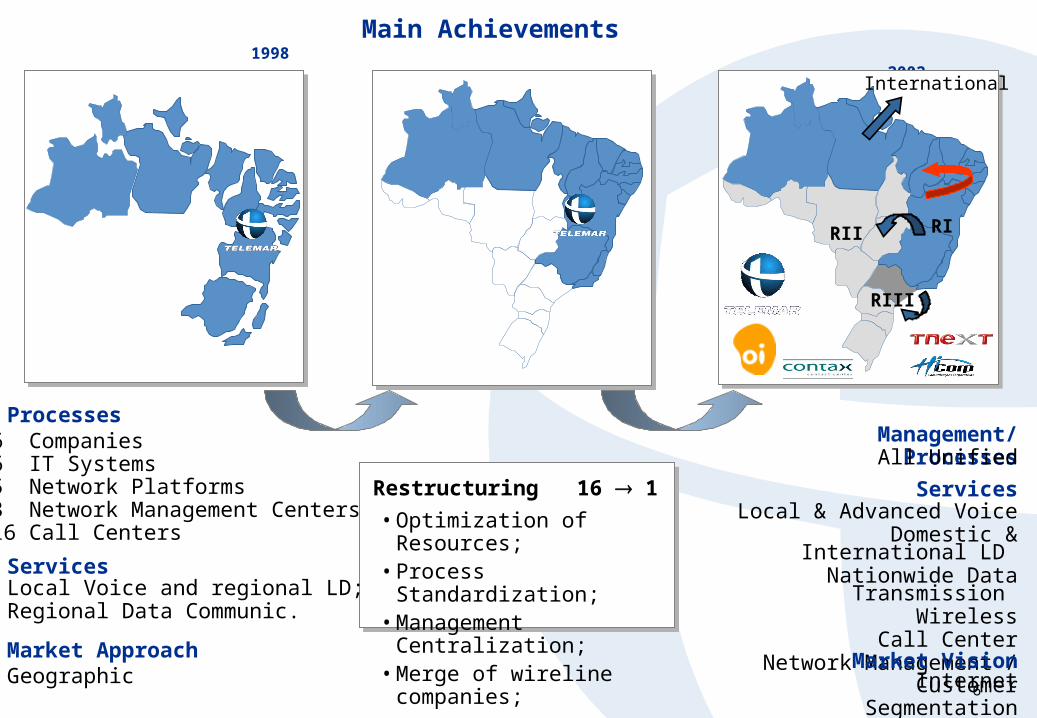

Main Achievements 1998 2002

Processes

Services

Market Approach

• Optimization of Resources;• Process Standardization;• Management Centralization;• Merge of wireline companies;

Restructuring 16 1

16 Companies 16 IT Systems 15 Network Platforms23 Network Management Centers116 Call Centers

Local Voice and regional LD;Regional Data Communic.

Geographic

Local & Advanced VoiceDomestic & International LD

Nationwide Data Transmission Wireless

Call CenterNetwork Management / Internet

Management/Processes

Services

Market VisionCustomer Segmentation

All Unified

International

RIII

RIRII

7

PLATFORM GROWTH – TMARMillion Lines in Service

+106%

7.27.8

9.7

11.8

14.8 14.615.1

Jul/98 1998 1999 2000 2001 Sep_01 Sep_02

8

+97%

* 1998, 1999 and 2000 refer to the Consolidated statement

6,946

5,158

8,433

6,222

10,851

8,127

13,687

10,133 9,997

7,391

11,573

8,516

1998* 1999* 2000* 2001 9M01 9M02

Gross Revenue Net Revenue

11,465

8,480

REVENUE GROWTH - TMARR$ Millions

9

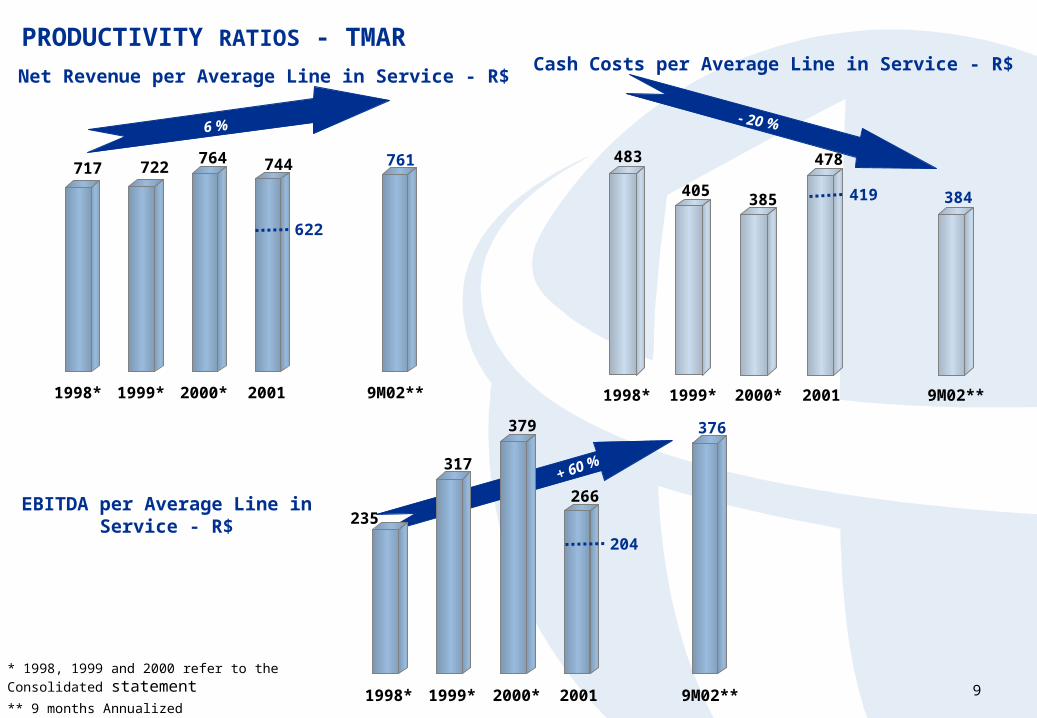

+ 60 %

6 %- 20 %

717 722764 744 761

1998* 1999* 2000* 2001 9M02**

483

405385

478

384

1998* 1999* 2000* 2001 9M02**

235

317

379

266

376

1998* 1999* 2000* 2001 9M02**

419

204

622

* 1998, 1999 and 2000 refer to the Consolidated statement** 9 months Annualized

EBITDA per Average Line in Service - R$

PRODUCTIVITY RATIOS - TMAR

Net Revenue per Average Line in Service - R$Cash Costs per Average Line in Service - R$

10

+ 342 %

322 397560

984

614

1,423

1998* 1999* 2000* 2001 9M01 9M02

+ 402 %

213255

385

673

1,069

1998* 1999* 2000* 2001 9M02**

70112

191

241

529

1998* 1999* 2000* 2001 9M02 **

184

563

+ 657 %

* 1998, 1999 and 2000 refer to the Consolidated statement** 9 months Annualized

EBITDA / Employee

(R$ Thousands)

EMPLOYEE PRODUCTIVITY - TMAR

Lines in Service / Employee

(R$ Thousands)

Net Revenue / Employee

(R$ Thousands)

11

CONSOLIDATED CAPEX - TNLR$ Millions

5 years R$ 19.0 bn

or US$ 9.6 bn

2,500 2,244 2,804

7,888

2,172

632702

1998 1999 2000 2001 9M02

Wireline Wireless

10,060

1,334

12

MANAGEMENT MODEL – MAIN PILLARS

Financial Management

Suppliers Management

Personnel Management

• Detailed Capex planning, cost and revenue matrix plan.• Strong cost control.• Strong budget control, focusing on return on investment/EVA.

• Meritocracy is key.• Talent management and retention of key personnel.• Culture based on corporate values and results oriented.• Formation of leaders and winning teams.• Quality management.• Strategic use of internal communication.

• Redesign of supply contracts, including quality and performance targets.

• Reduction of the supplier base and centralized management.• Development of strategic suppliers.• Outsoursing of non-core activities (call center, etc).• Consolidation of network technologies.

Corporate Management

• Specific targets broken-down to all management levels.• Monthly evaluation.• Simple structure with few hierarchic levels.• Redesign and standardization of key processes.• Variable remuneration based on achievement of targets.• Thematic decision making Committees.

13

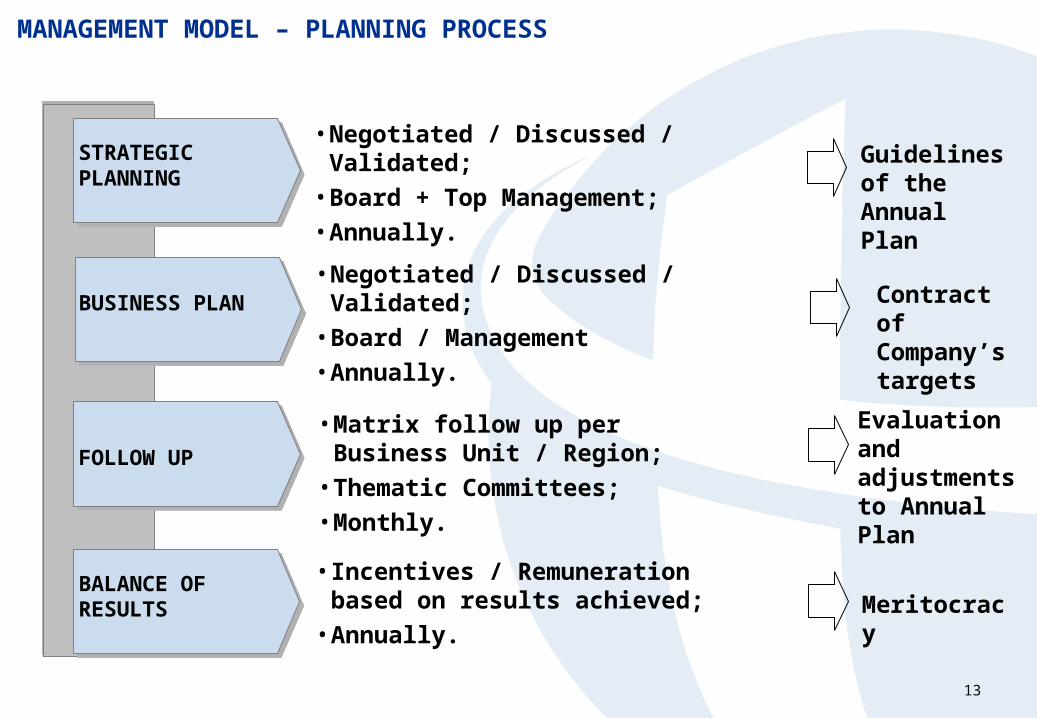

MANAGEMENT MODEL – PLANNING PROCESS

STRATEGIC PLANNING

FOLLOW UP

BUSINESS PLAN

• Negotiated / Discussed / Validated;

• Board + Top Management;

• Annually.

• Negotiated / Discussed / Validated;

• Board / Management

• Annually.

• Matrix follow up per Business Unit / Region;

• Thematic Committees;

• Monthly.

BALANCE OF RESULTS

• Incentives / Remuneration based on results achieved;

• Annually.

Guidelines of the Annual Plan

Contract of Company’s targets

Evaluation and adjustments to Annual Plan

Meritocracy

14

Part III

Achievements and Challenges

16

Achievements

Better than expected launching of a huge GSM startup;

Launching of a new brand, with a strong appeal to life style, with a different proposition to the market; cellular treated as a personal consumer product, instead of a telecommunication product;

500,000 clients in three months attracted by innovative marketing campaigns;

First GSM company in Brazil, with advantages in relation to incumbents such as worldwide handset scale, higher flexibility and security to customer, more sophisticated products and services;

Focus on innovative products and services (voice and data).

17

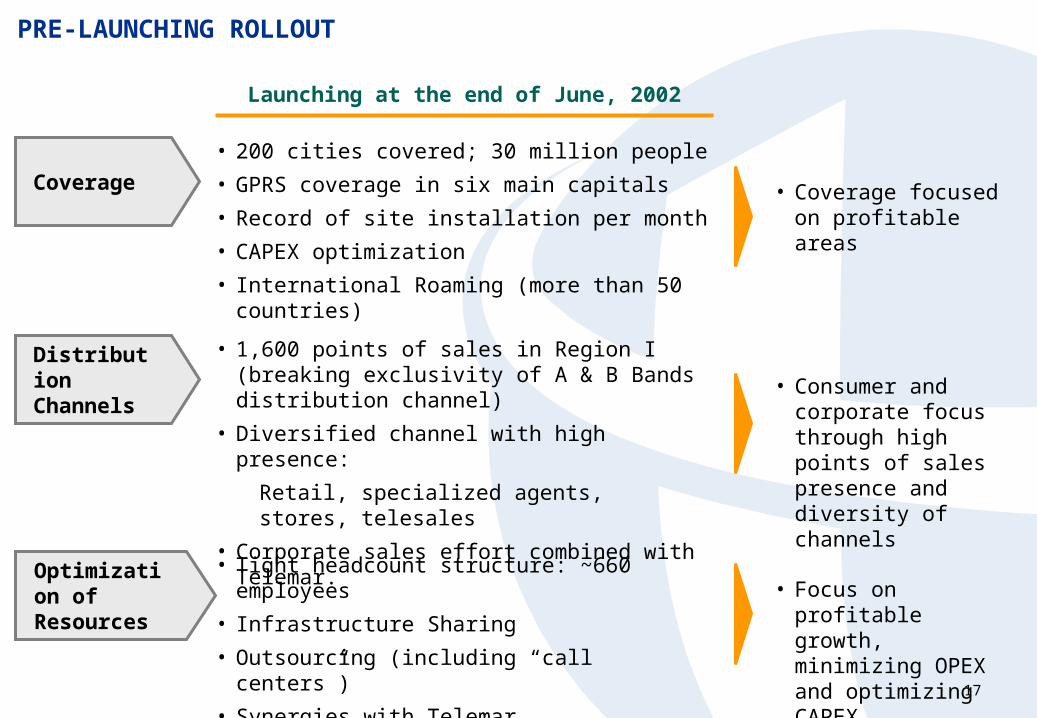

PRE-LAUNCHING ROLLOUT

Launching at the end of June, 2002

Coverage

• 200 cities covered; 30 million people

• GPRS coverage in six main capitals

• Record of site installation per month

• CAPEX optimization

• International Roaming (more than 50 countries)

• Coverage focused on profitable areas

Distribution Channels

• 1,600 points of sales in Region I (breaking exclusivity of A & B Bands distribution channel)

• Diversified channel with high presence:

Retail, specialized agents, stores, telesales

• Corporate sales effort combined with Telemar.

• Consumer and corporate focus through high points of sales presence and diversity of channels

Optimization of Resources

• Tight headcount structure: ~660 employees

• Infrastructure Sharing

• Outsourcing (including “call centers”)

• Synergies with Telemar.

• Focus on profitable growth, minimizing OPEX and optimizing CAPEX

18

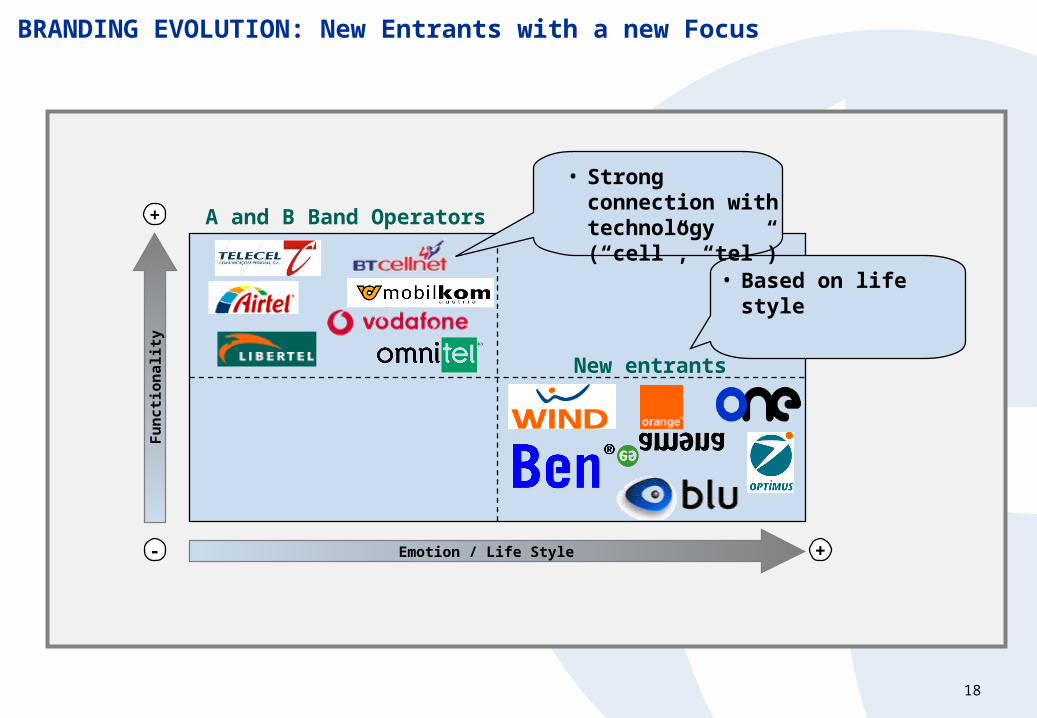

BRANDING EVOLUTION: New Entrants with a new Focus

Fu

nct

ion

alit

y

Emotion / Life Style-

+

+

A and B Band Operators

New entrants

• Strong connection with technology (“cell”, “tel”)

• Based on life style

19

Oi BRANDING

Instead of emphasizing Tel and Cell... ... focused on goods and emotions

20

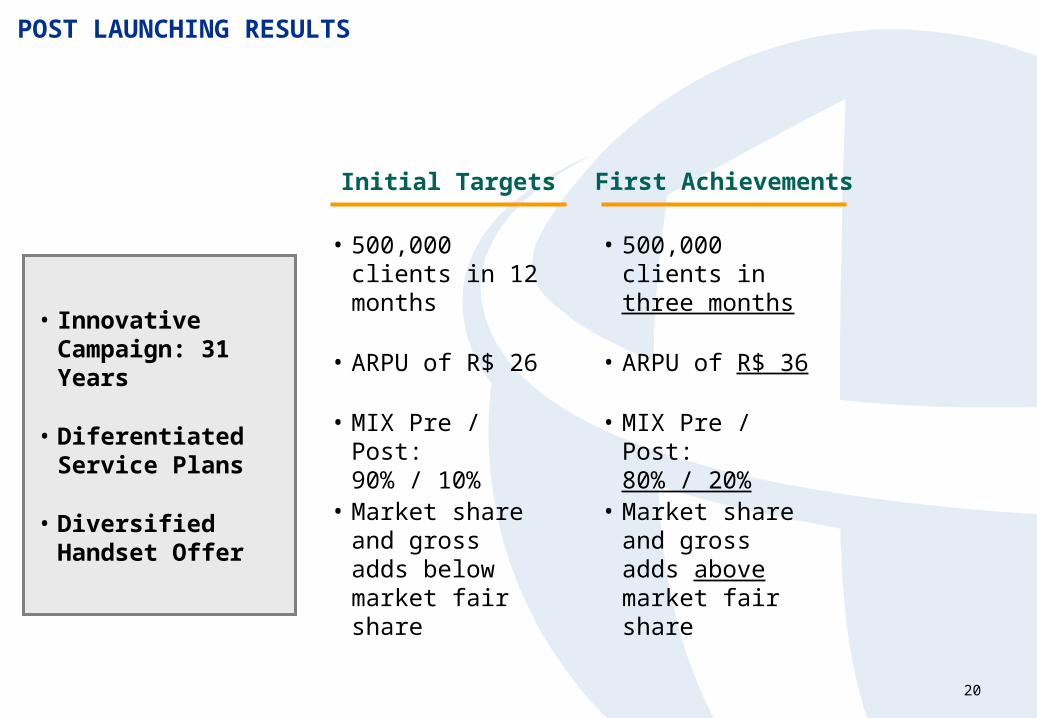

POST LAUNCHING RESULTS

• Innovative Campaign: 31 Years

• Diferentiated Service Plans

• Diversified Handset Offer

Initial Targets

• 500,000 clients in 12 months

• ARPU of R$ 26

• MIX Pre / Post: 90% / 10%

• Market share and gross adds below market fair share

First Achievements

• 500,000 clients in three months

• ARPU of R$ 36

• MIX Pre / Post: 80% / 20%

• Market share and gross adds above market fair share

21

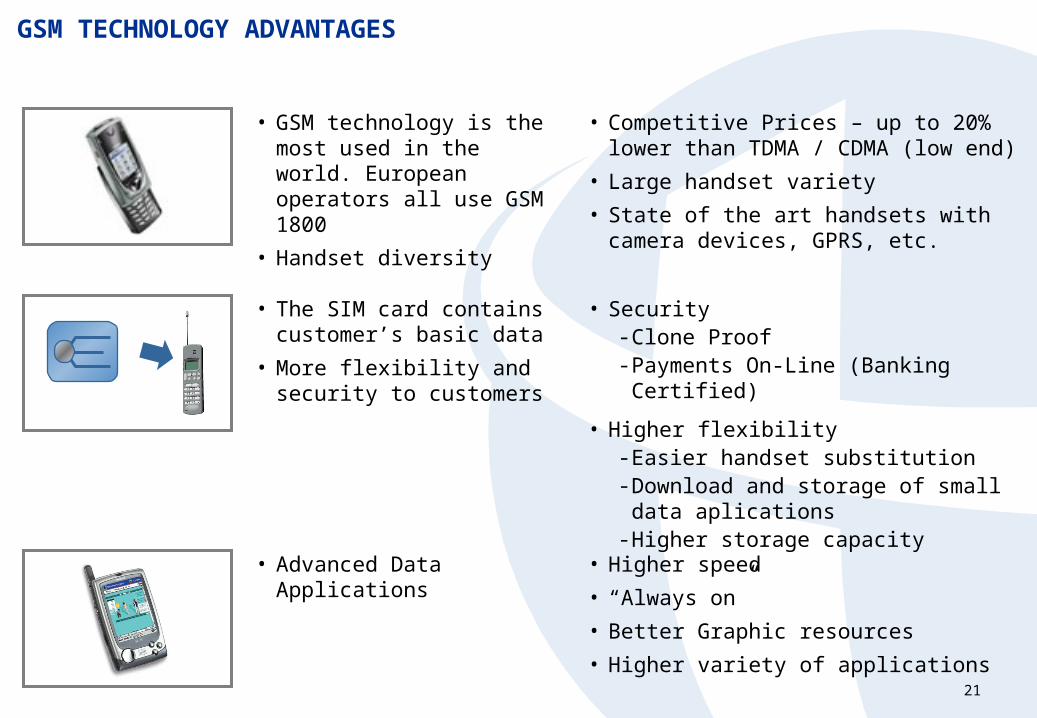

GSM TECHNOLOGY ADVANTAGES

• GSM technology is the most used in the world. European operators all use GSM 1800

• Handset diversity

• Competitive Prices – up to 20% lower than TDMA / CDMA (low end)

• Large handset variety

• State of the art handsets with camera devices, GPRS, etc.

• The SIM card contains customer’s basic data

• More flexibility and security to customers

• Security- Clone Proof- Payments On-Line (Banking Certified)

• Higher flexibility- Easier handset substitution - Download and storage of small data

aplications- Higher storage capacity

• Advanced Data Applications • Higher speed

• “Always on”

• Better Graphic resources

• Higher variety of applications

22

Oi MTV Product

Services

Plans

Handsets

Packs / Bundles

Devices

• Increased customer base

• Stimulated Voice Usage

• Stronger SMS usage

• Brand Name Consolidation

• Very positive initial results

23

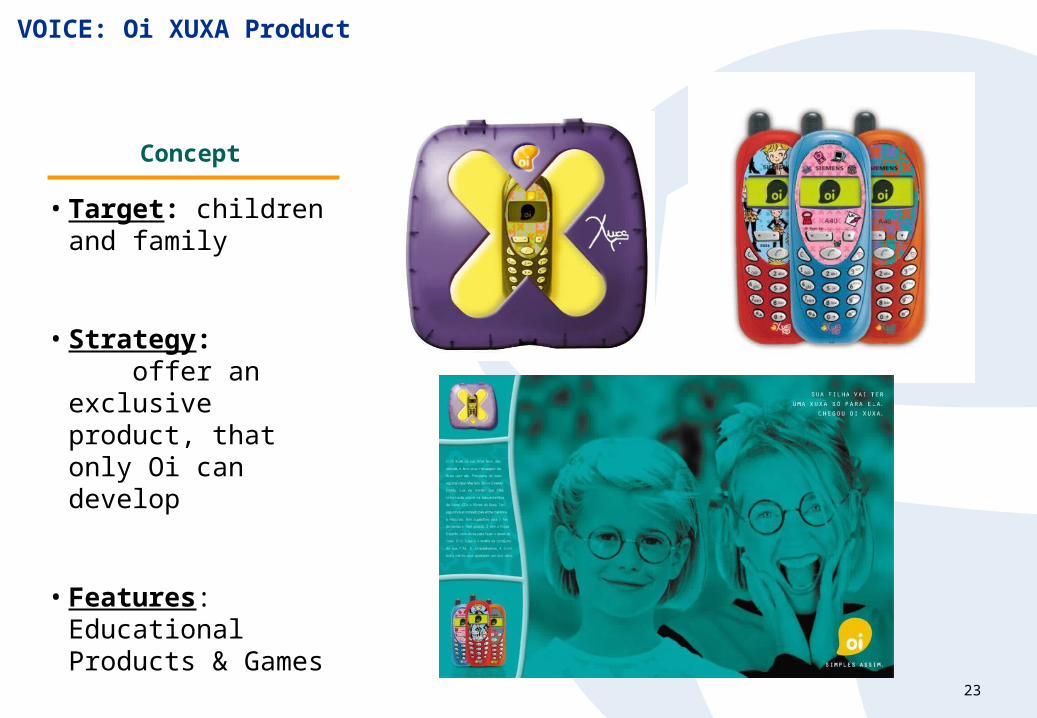

VOICE: Oi XUXA Product

Concept

• Target: children and family

• Strategy: offer an exclusive product, that only Oi can develop

• Features: Educational Products & Games

• Focus: Continued Service

24

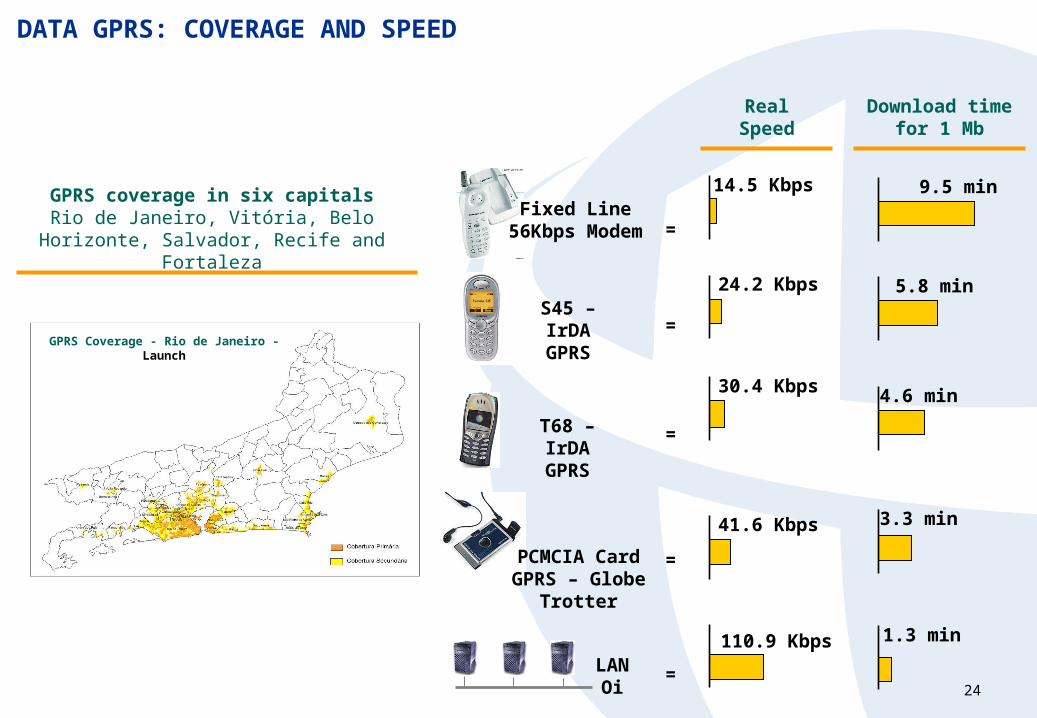

DATA GPRS: COVERAGE AND SPEED

GPRS coverage in six capitalsRio de Janeiro, Vitória, Belo Horizonte,

Salvador, Recife and Fortaleza

Fixed Line56Kbps Modem =

9.5 min14.5 Kbps

S45 – IrDAGPRS =

5.8 min24.2 Kbps

T68 – IrDAGPRS

=

4.6 min30.4 Kbps

PCMCIA CardGPRS – Globe

Trotter

=

3.3 min41.6 Kbps

LAN Oi =

1.3 min110.9 Kbps

Real Speed

Download time for 1 Mb

GPRS Coverage - Rio de Janeiro - Launch

25

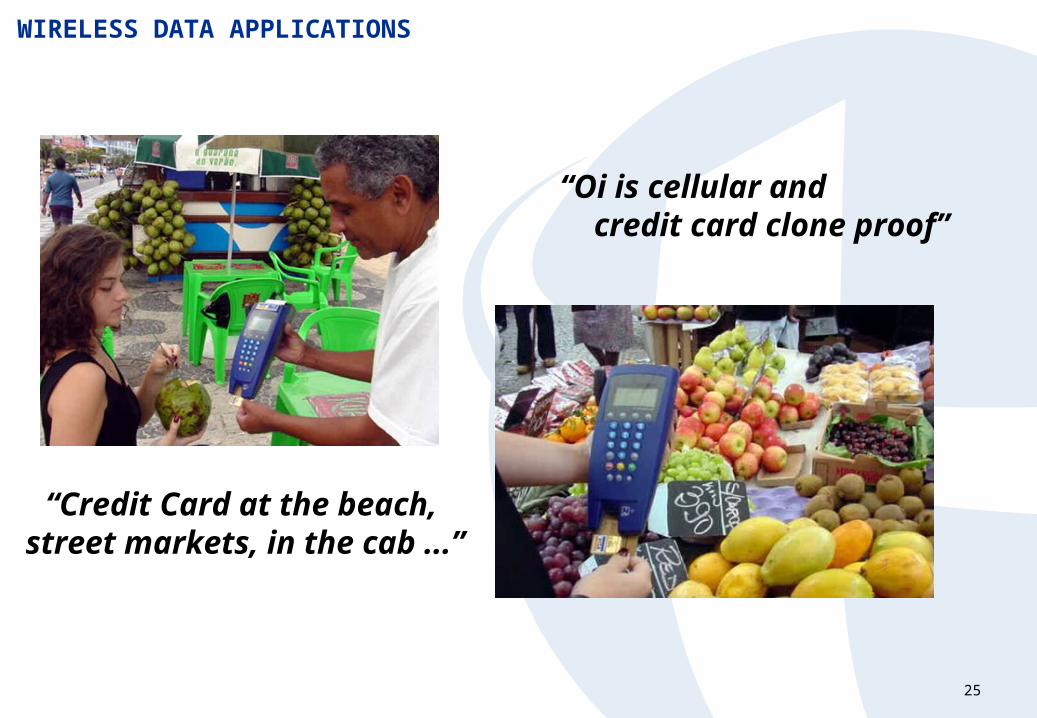

“Oi is cellular and credit card clone proof”

“Credit Card at the beach, street markets, in the cab ...”

WIRELESS DATA APPLICATIONS

26

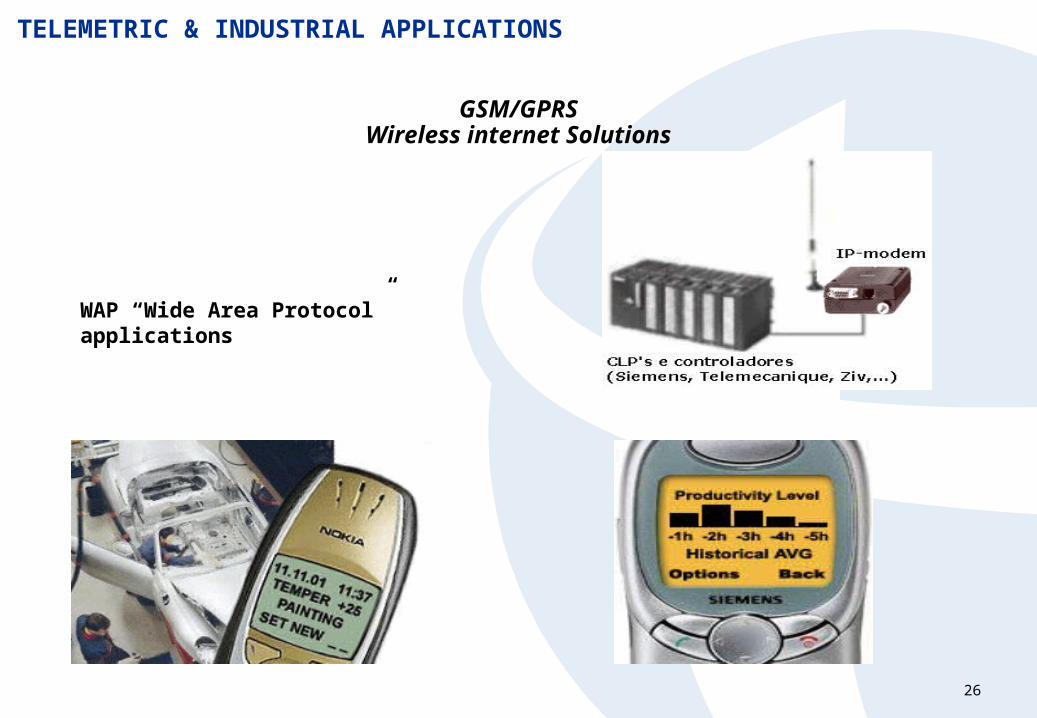

TELEMETRIC & INDUSTRIAL APPLICATIONS

WAP “Wide Area Protocol” applications

GSM/GPRSWireless internet Solutions

27

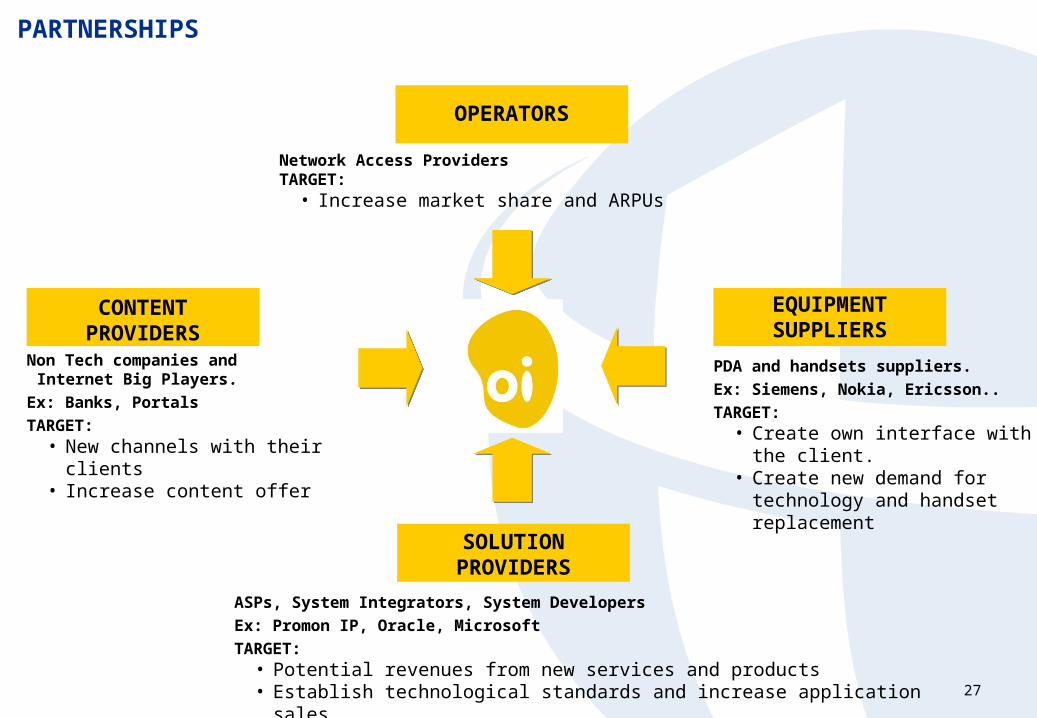

PARTNERSHIPS

OPERATORS

SOLUTION PROVIDERS

CONTENT PROVIDERS

Non Tech companies and Internet Big Players.

Ex: Banks, Portals

TARGET:• New channels with their clients• Increase content offer

EQUIPMENT SUPPLIERS

PDA and handsets suppliers.

Ex: Siemens, Nokia, Ericsson..

TARGET:• Create own interface with the

client.• Create new demand for

technology and handset replacement

ASPs, System Integrators, System Developers

Ex: Promon IP, Oracle, Microsoft

TARGET:• Potential revenues from new services and products • Establish technological standards and increase application sales.

Network Access ProvidersTARGET:

• Increase market share and ARPUs

28

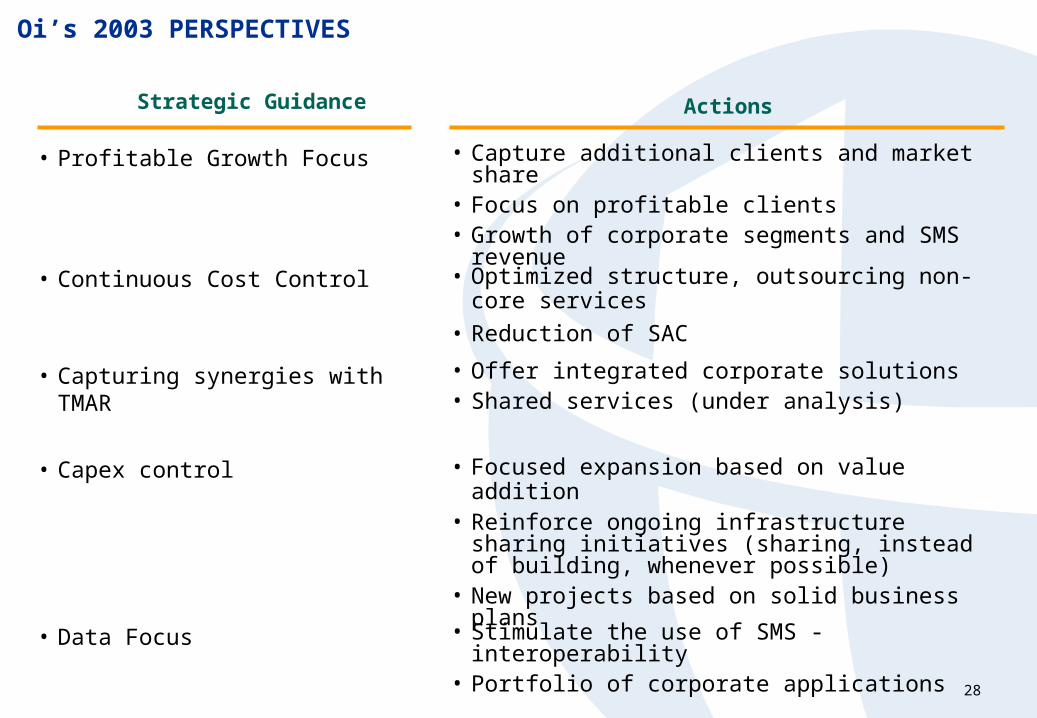

ActionsStrategic Guidance

• Capture additional clients and market share• Focus on profitable clients• Growth of corporate segments and SMS revenue

• Profitable Growth Focus

• Optimized structure, outsourcing non-core services

• Reduction of SAC• Continuous Cost Control

• Offer integrated corporate solutions • Shared services (under analysis)

• Capturing synergies with TMAR

• Focused expansion based on value addition• Reinforce ongoing infrastructure sharing initiatives

(sharing, instead of building, whenever possible)• New projects based on solid business plans

• Capex control

• Stimulate the use of SMS - interoperability• Portfolio of corporate applications

• Data Focus

Oi’s 2003 PERSPECTIVES

EASY AS IT IS!

30

Part IV

FINANCIAL RESULTS

31

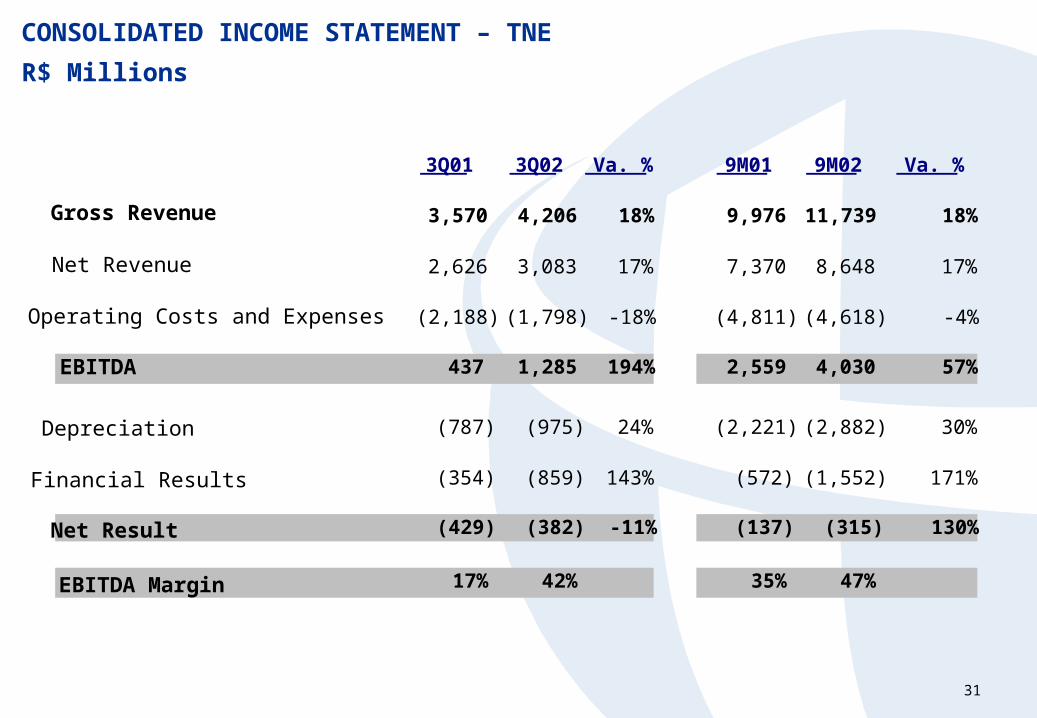

3Q01 3Q02 Va. % 9M01 9M02 Va. %

3,570 4,206 18% 9,976 11,739 18%

2,626 3,083 17% 7,370 8,648 17%

(2,188) (1,798) -18% (4,811) (4,618) -4%

437 1,285 194% 2,559 4,030 57%

(787) (975) 24% (2,221) (2,882) 30%

(354) (859) 143% (572) (1,552) 171%

(429) (382) -11% (137) (315) 130%

17% 42% 35% 47%

Gross Revenue

Net Revenue

Operating Costs and Expenses

EBITDA

Depreciation

Financial Results

Net Result

EBITDA Margin

CONSOLIDATED INCOME STATEMENT – TNE

R$ Millions

32

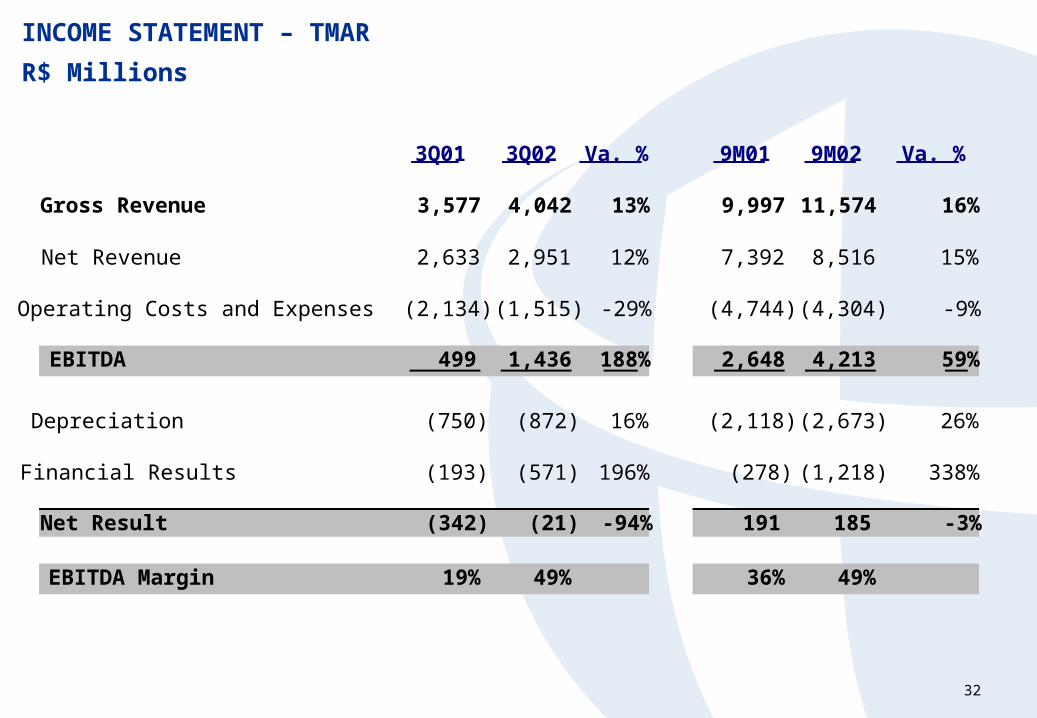

INCOME STATEMENT – TMAR

R$ Millions

3Q01 3Q02 Va. % 9M01 9M02 Va. %

Gross Revenue 3,577 4,042 13% 9,997 11,574 16%

Net Revenue 2,633 2,951 12% 7,392 8,516 15%

Operating Costs and Expenses (2,134) (1,515) -29% (4,744) (4,304) -9%

EBITDA 499 1,436 188% 2,648 4,213 59%

Depreciation (750) (872) 16% (2,118) (2,673) 26%

Financial Results (193) (571) 196% (278) (1,218) 338%

Net Result (342) (21) -94% 191 185 -3%

EBITDA Margin 19% 49% 36% 49%

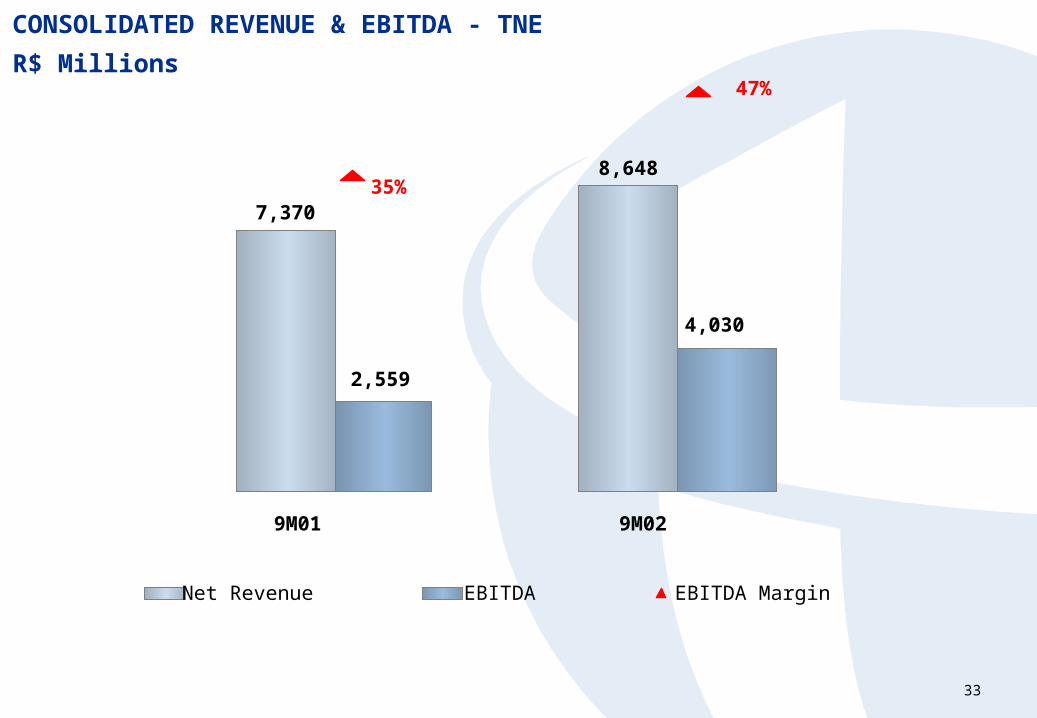

33

CONSOLIDATED REVENUE & EBITDA - TNE

R$ Millions

7,370

8,648

4,030

2,559

47%

35%

9M01 9M02

Net Revenue EBITDA EBITDA Margin

34

CONSOLIDATED CAPEX - TNER$ Millions

2,000

6,222

8,1228,648

10,060

1.334

7,058

2,8042,2442,500

7,370

5,158

10,103

1998 1999 2000 2001 9M01 9M02 2002E

Capex Net Revenue

CAPEX / Net Revenue (%)

96%

17%

48%

36% 35%

100%

15%

1998 1999 2000 2001 9M01 9M02 2002E

35

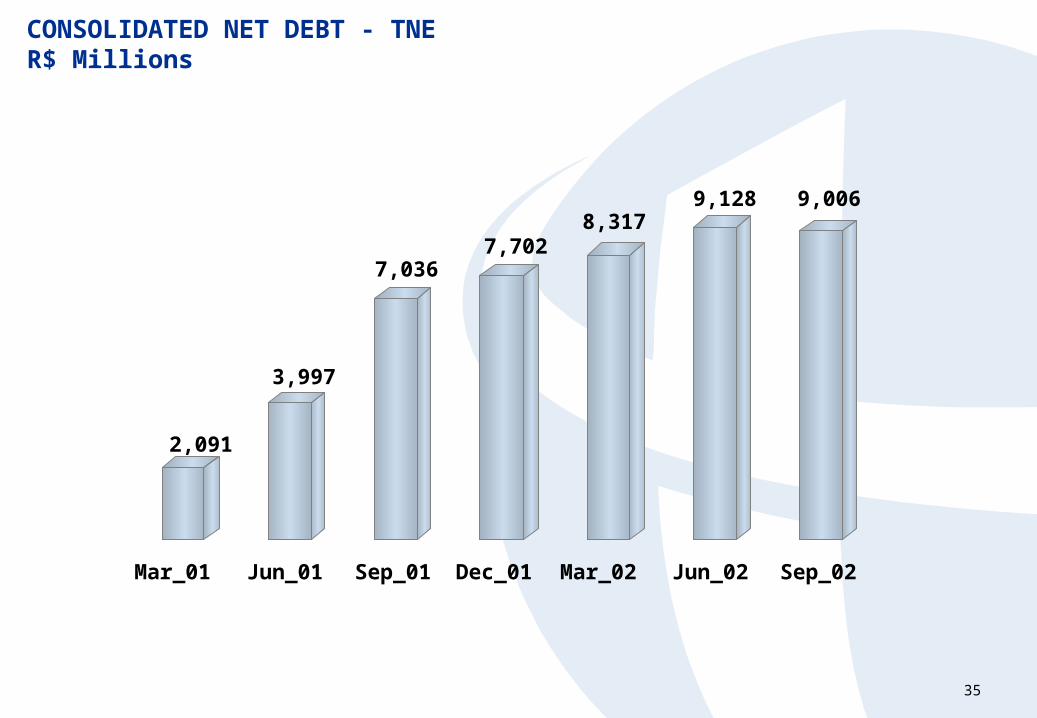

CONSOLIDATED NET DEBT - TNER$ Millions

2,091

3,997

7,0367,702

8,3179,128 9,006

Mar_01 Jun_01 Sep_01 Dec_01 Mar_02 Jun_02 Sep_02

36

CONSOLIDATED DEBT – CURRENCY AND COST (SEP/02)

Currency

46%

11%

10%

33%

Domestic

US$

Yen (Swap to US$)

Currency

Basket

52%

15%

20%

13% CDI

TJLP

Floating Rate (US$)

Interest

Currency Cost (% p.a.)US$ Libor + 5 Yen 1.7

Basket 12.3Real 16.0

Cost of Debt

Fixed Rate (US$)

37

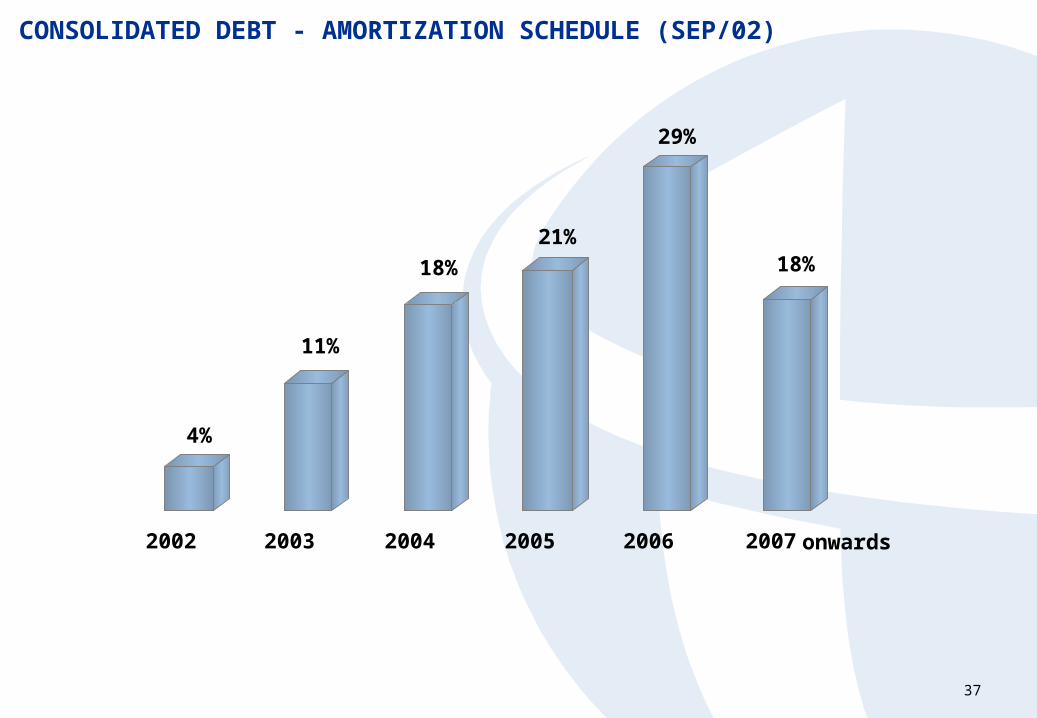

CONSOLIDATED DEBT - AMORTIZATION SCHEDULE (SEP/02)

4%

11%

18%

21%

29%

18%

2002 2003 2004 2005 2006 2007 onwards

38

This presentation contains forward-looking statements. Statements that are not historical facts, including

statements about our beliefs and expectations, are forward-looking statements and involve inherent risks

and uncertainties. These statements are based on current plans, estimates and projections, and therefore

you should not place undue reliance on them. Forward-looking statements speak only as of the date they

are made, and we undertake no obligation to update publicly any of them in light of new information or

future events.

““SAFE HARBOR” STATEMENTSAFE HARBOR” STATEMENT

Investor Relations

Rua Humberto de Campos, 425 / 8º andar

Leblon

Rio de Janeiro -RJ

Phone: ( 55 21) 3131-1314/1313/1315/1316/1317

Fax: (55 21) 3131-1155

E-mail: [email protected]

Visit our website: http://www.telemar.com.br/ri