TELE NORTE LESTE PARTICIPAÇÕES S.A.

25

December/02 1 TELE NORTE LESTE PARTICIPAÇÕES S.A. TELE NORTE LESTE PARTICIPAÇÕES S.A.

-

Upload

julian-zamora -

Category

Documents

-

view

40 -

download

0

description

TELE NORTE LESTE PARTICIPAÇÕES S.A. Overview – September / 2002. Largest Integrated Telecom Company in Brazil 15.1 million fixed lines in service 978,000 mobile subscribers (Nov/02) Concession Area: 65% of Brazilian Territory / 93 million people 40% of Country’s GDP - PowerPoint PPT Presentation

Transcript of TELE NORTE LESTE PARTICIPAÇÕES S.A.

December/021

TELE NORTE LESTE PARTICIPAÇÕES S.A.TELE NORTE LESTE PARTICIPAÇÕES S.A.

December/022

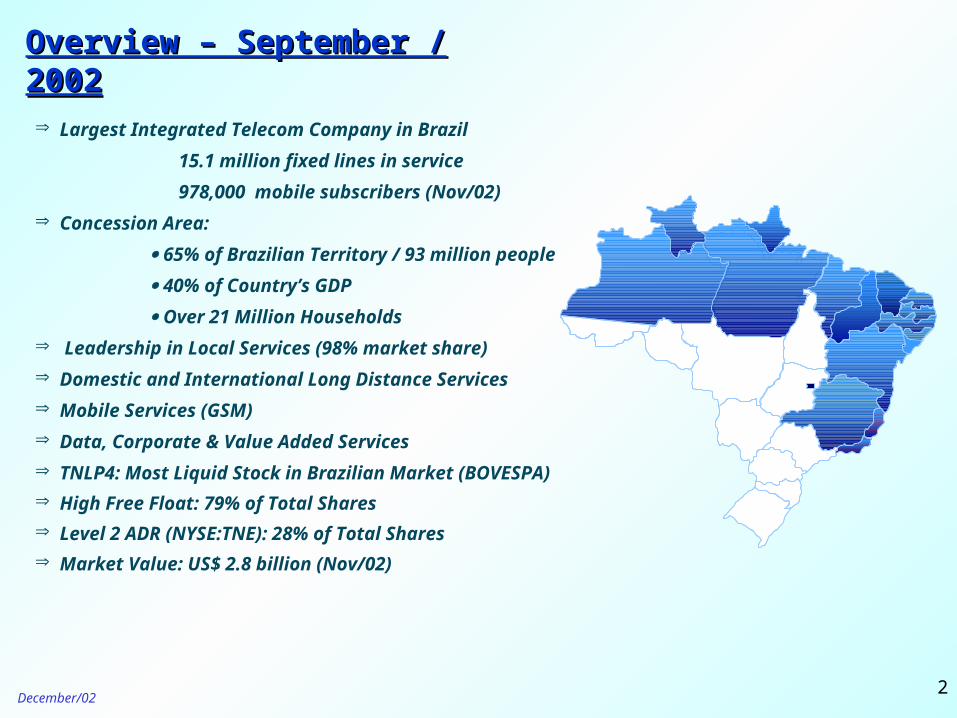

Largest Integrated Telecom Company in Brazil

15.1 million fixed lines in service

978,000 mobile subscribers (Nov/02)

Concession Area:

65% of Brazilian Territory / 93 million people

40% of Country’s GDP

Over 21 Million Households

Leadership in Local Services (98% market share)

Domestic and International Long Distance Services

Mobile Services (GSM)

Data, Corporate & Value Added Services

TNLP4: Most Liquid Stock in Brazilian Market (BOVESPA)

High Free Float: 79% of Total Shares

Level 2 ADR (NYSE:TNE): 28% of Total Shares

Market Value: US$ 2.8 billion (Nov/02)

Overview – September / 2002Overview – September / 2002

December/023

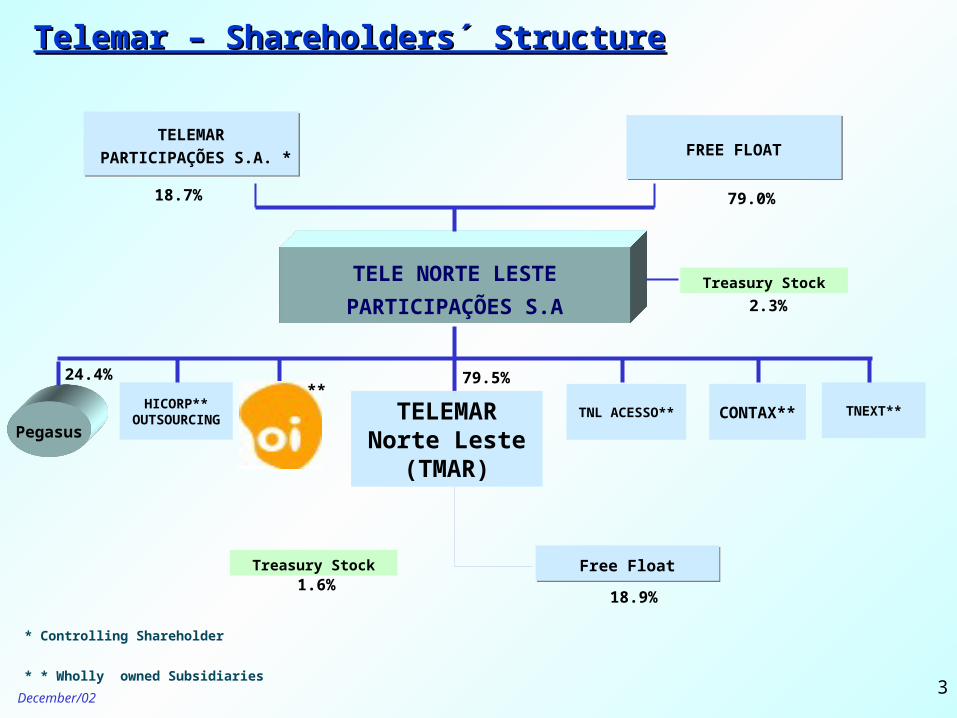

TELE NORTE LESTE

PARTICIPAÇÕES S.A

79.0% 18.7%

HICORP**OUTSOURCING TNL ACESSO** CONTAX** TNEXT**

TELEMAR

PARTICIPAÇÕES S.A. *

TELEMAR

PARTICIPAÇÕES S.A. *

TELEMARNorte Leste

(TMAR)

Treasury Stock

79.5%

Free FloatFree Float

18.9%

Treasury Stock

FREE FLOATFREE FLOAT

Pegasus

Telemar – Shareholders´ StructureTelemar – Shareholders´ Structure

* Controlling Shareholder

* * Wholly owned Subsidiaries

24.4%

2.3%

1.6%

**

December/024

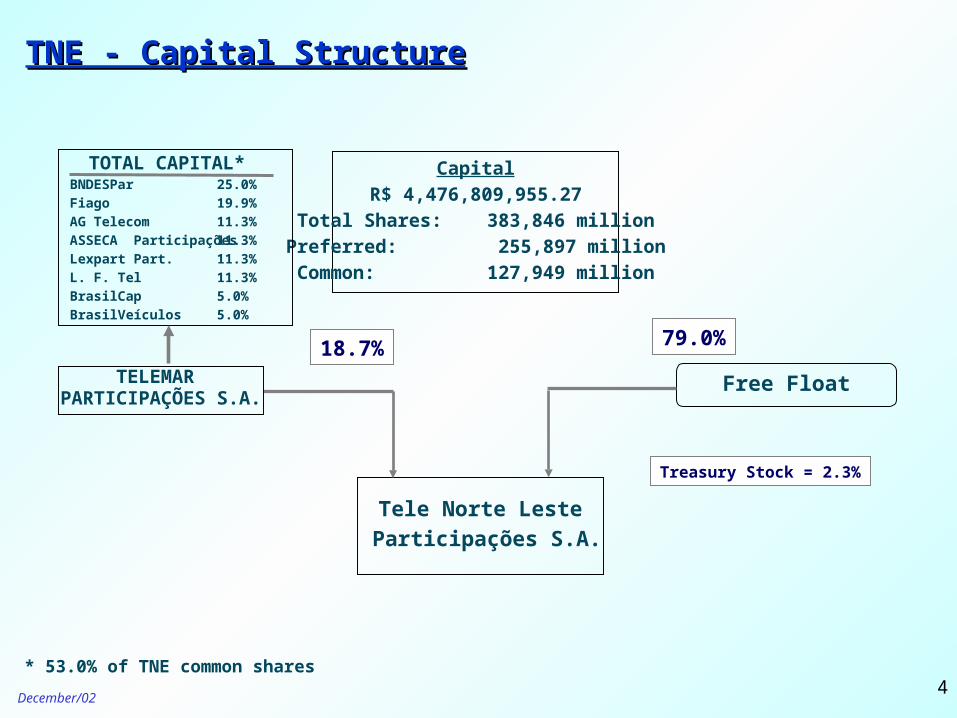

TNE - Capital StructureTNE - Capital Structure

Tele Norte Leste

Participações S.A.

Free Float

79.0%18.7%TELEMAR

PARTICIPAÇÕES S.A.

Capital

R$ 4,476,809,955.27

Total Shares: 383,846 million

Preferred: 255,897 million

Common: 127,949 million

Treasury Stock = 2.3%

TOTAL CAPITAL*BNDESPar

Fiago

AG Telecom

ASSECA Participações

Lexpart Part.

L. F. Tel

BrasilCap

BrasilVeículos

25.0%

19.9%

11.3%

11.3%

11.3%

11.3%

5.0%

5.0%

* 53.0% of TNE common shares

December/025

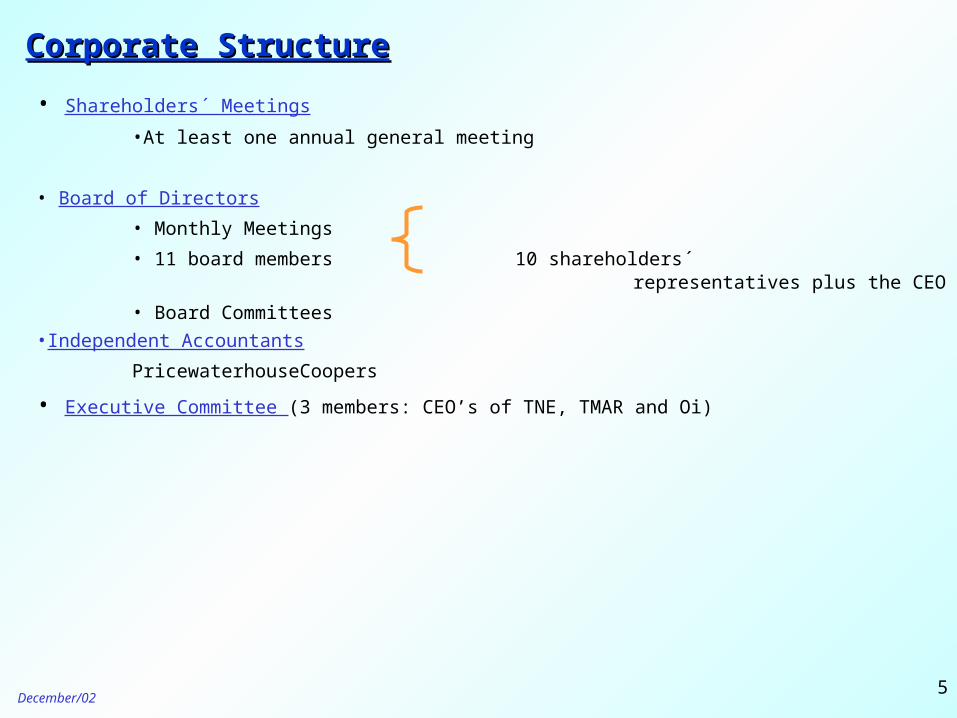

• Shareholders´ Meetings

•At least one annual general meeting

• Board of Directors

• Monthly Meetings

• 11 board members 10 shareholders´ representatives plus the CEO

• Board Committees

•Independent Accountants

PricewaterhouseCoopers

• Executive Committee (3 members: CEO’s of TNE, TMAR and Oi)

Corporate StructureCorporate Structure

December/026

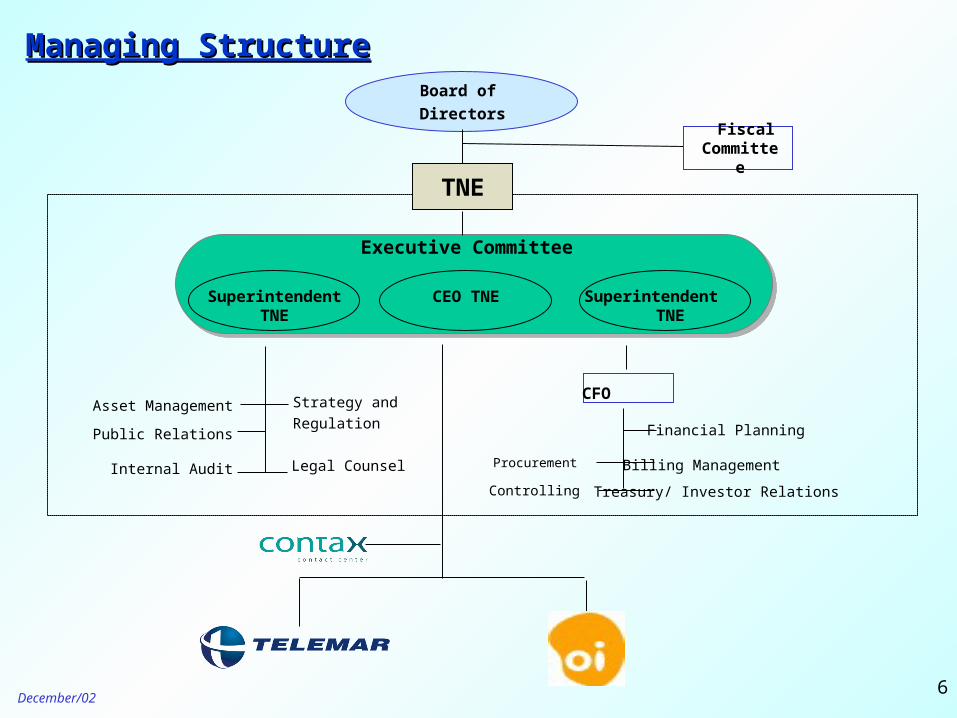

Managing StructureManaging Structure

Fiscal Committee

Board of

Directors

TNE

Executive Committee

Controlling

Procurement

Treasury/ Investor Relations

CFOStrategy and

Regulation

Legal Counsel

Financial Planning

Asset Management

Public Relations

Billing ManagementInternal Audit

Superintendent TNE

SuperintendentTNE

CEO TNE

December/027

Universal Service

Targets

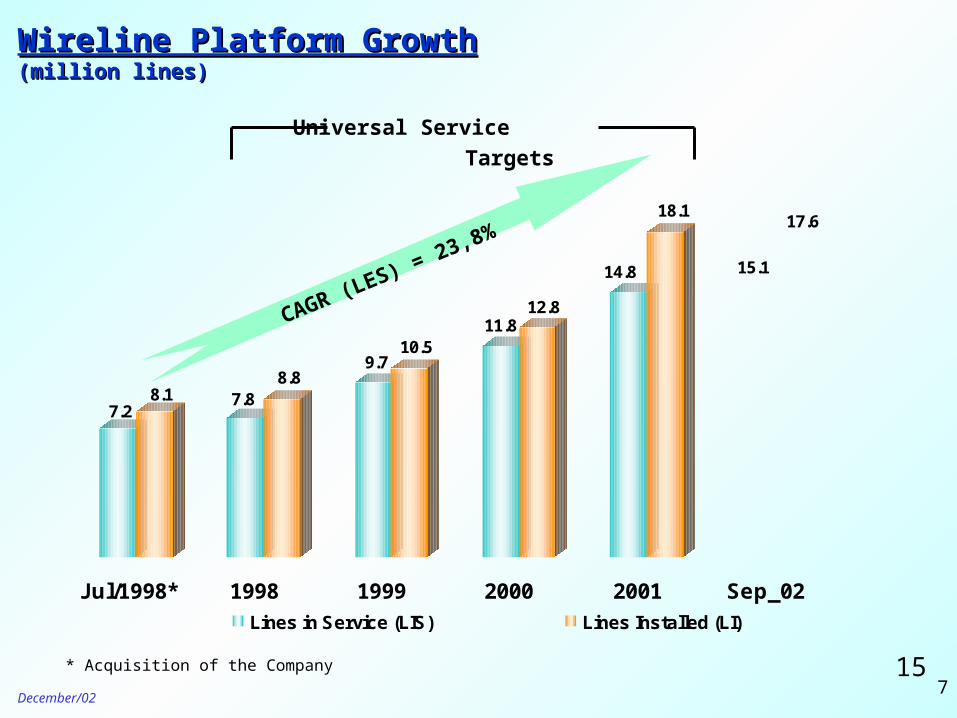

Wireline Platform GrowthWireline Platform Growth(million lines)(million lines)

* Acquisition of the Company

CAGR (LES) = 23,8%

15

7.28.1 7.8

8.89.7

10.511.8

12.8

14.8

18.1

15.1

17.6

Jul/1998* 1998 1999 2000 2001 Sep_02

Lines in Service (LIS) Lines Installed (LI)

December/028

6,946

5,158

8,433

6,222

10,851

8,122

13,660

10,103 9,976

7,370

11,739

8,648

1998 1999 2000 2001 9M01 9M02

Gross Revenue Net Revenue

Revenue GrowthRevenue Growth(R$ Mn)(R$ Mn)

Net Revenue

CAGR = 25.1%

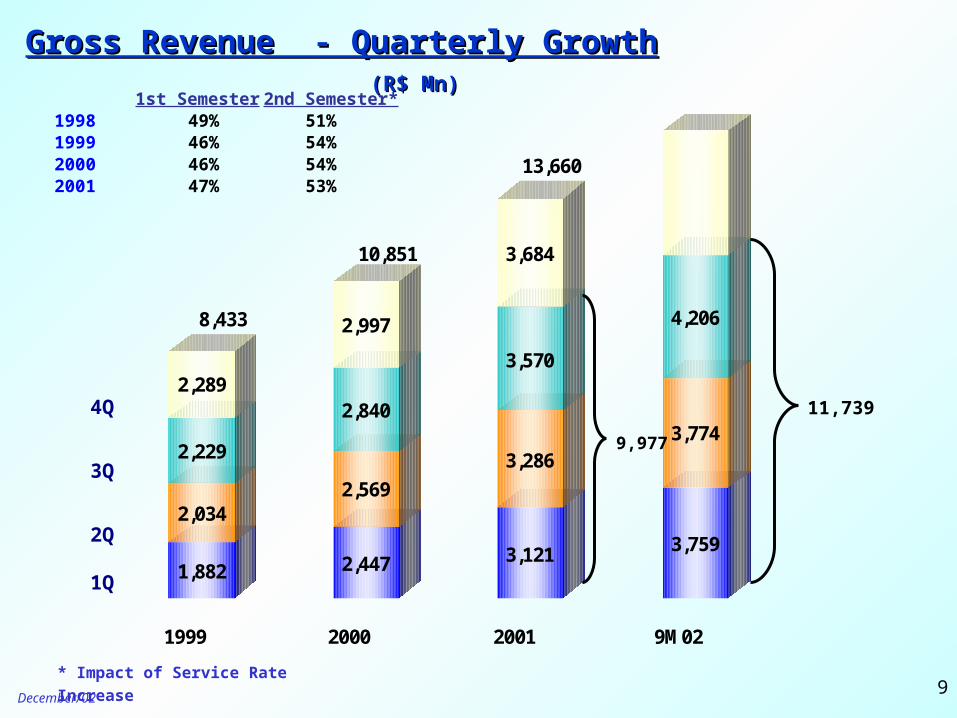

December/029

1,882

2,034

2,229

2,289

2,447

2,569

2,840

2,997

3,121

3,286

3,570

3,684

3,759

3,774

4,206

1999 2000 2001 9M02

8,433

10,851

13,660

Gross Revenue - Quarterly GrowthGross Revenue - Quarterly Growth (R$ Mn)(R$ Mn)

3Q

1Q

2Q

4Q

1st Semester 2nd Semester*1998 49% 51%1999 46% 54%2000 46% 54%2001 47% 53%

* Impact of Service Rate Increase

11,739

9,977

December/0210

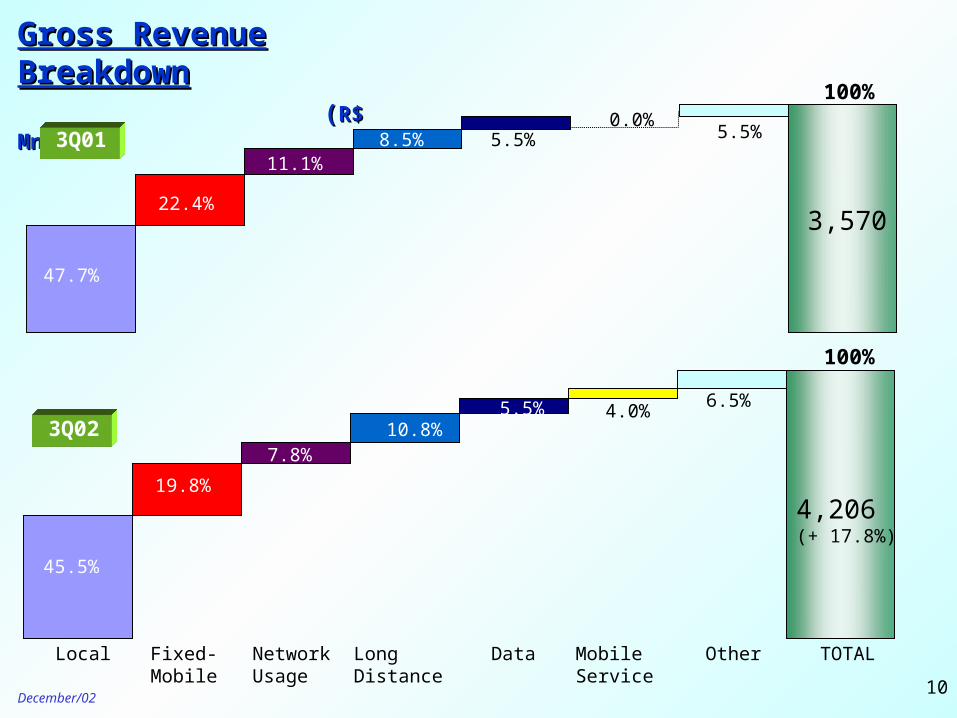

Gross Revenue BreakdownGross Revenue Breakdown ((R$ Mn)R$ Mn)

100%

3Q01

3,570

47.7%

22.4%

11.1% 8.5% 5.5%

5.5%0.0%

100%

3Q02

45.5%

19.8%

7.8% 10.8%

5.5% 4.0%6.5%

4,206(+ 17.8%)

Local Fixed-Mobile

Network Usage

LongDistance

Data MobileService

Other TOTAL

December/0211

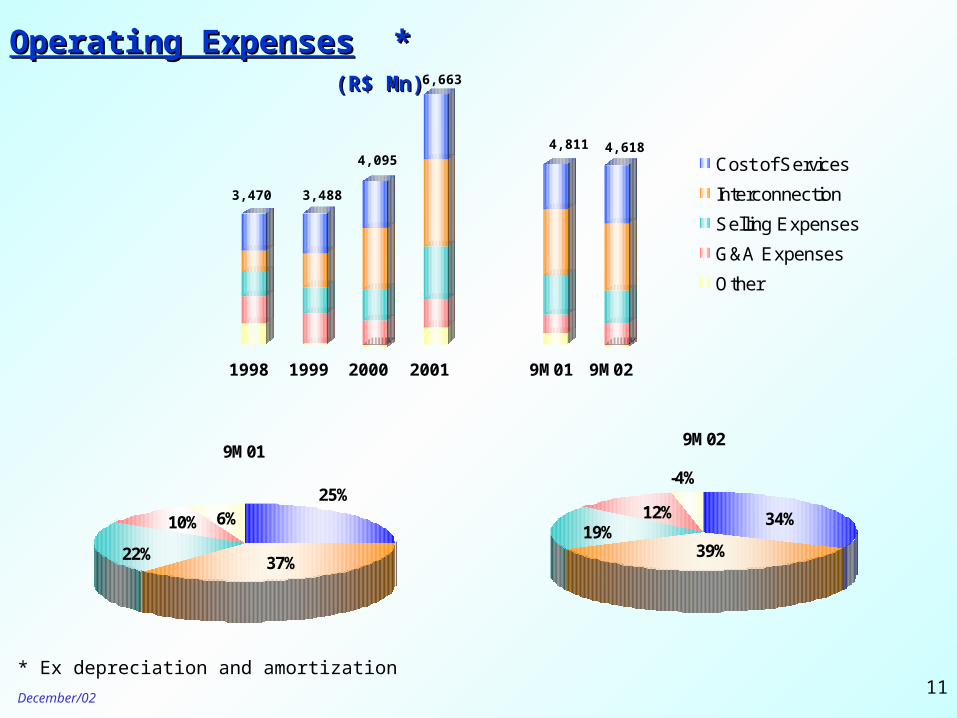

Operating ExpensesOperating Expenses * * (R$ Mn) (R$ Mn)

3,470 3,488

4,095

6,663

4,6184,811

9M01

6%25%

10%

22% 37%

9M02

-4%

34%12%

39%19%

1998 1999 2000 2001 9M01 9M02

Cost of Services

Interconnection

Selling Expenses

G&A Expenses

Other

* Ex depreciation and amortization

December/0212

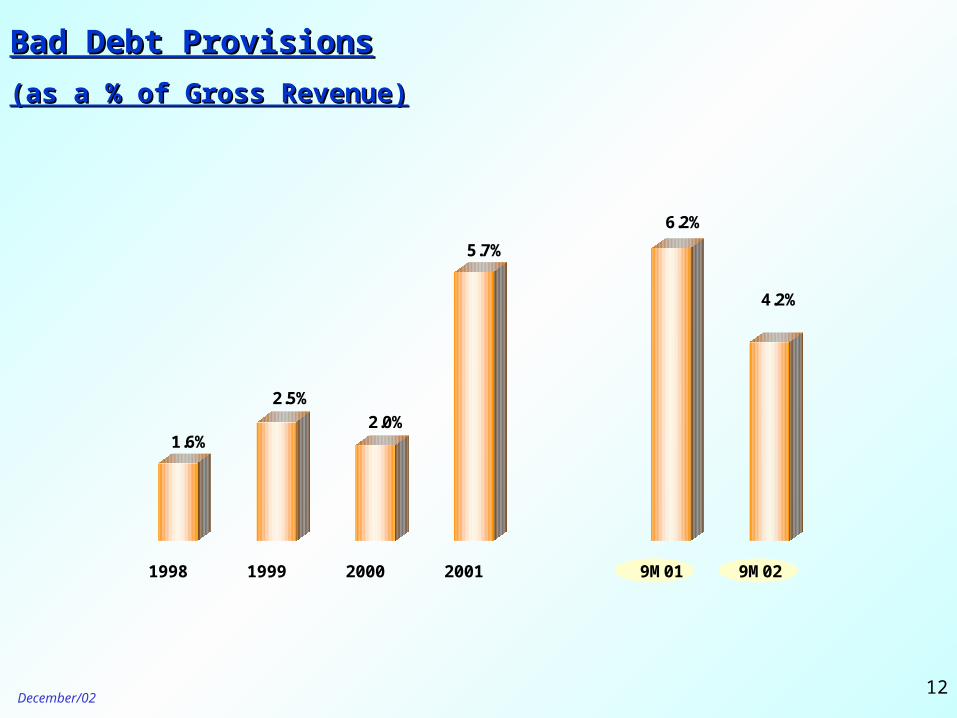

Bad Debt ProvisionsBad Debt Provisions

(as a % of Gross Revenue)(as a % of Gross Revenue)

1.6%

2.5%

2.0%

5.7%

6.2%

4.2%

1998 1999 2000 2001 9M01 9M02

December/0213

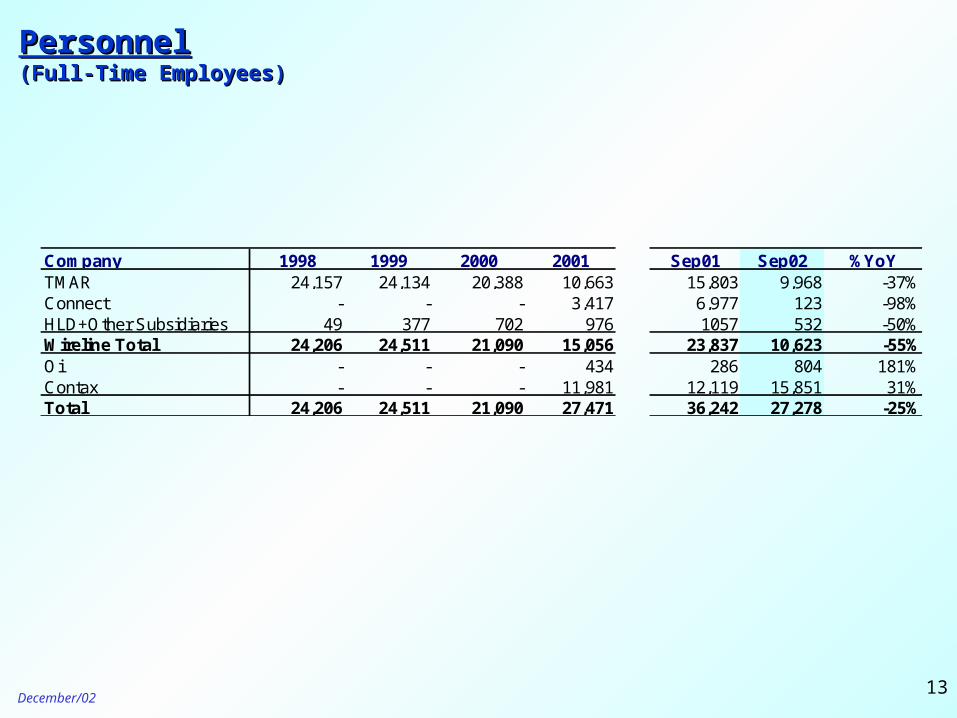

PersonnelPersonnel(Full-Time Employees)(Full-Time Employees)

Company 1998 1999 2000 2001 Sep01 Sep02 %YoYTMAR 24,157 24,134 20,388 10,663 15,803 9,968 -37%Connect - - - 3,417 6,977 123 -98%HLD+Other Subsidiaries 49 377 702 976 1057 532 -50%Wireline Total 24,206 24,511 21,090 15,056 23,837 10,623 -55%Oi - - - 434 286 804 181%Contax - - - 11,981 12,119 15,851 31%Total 24,206 24,511 21,090 27,471 36,242 27,278 -25%

December/0214

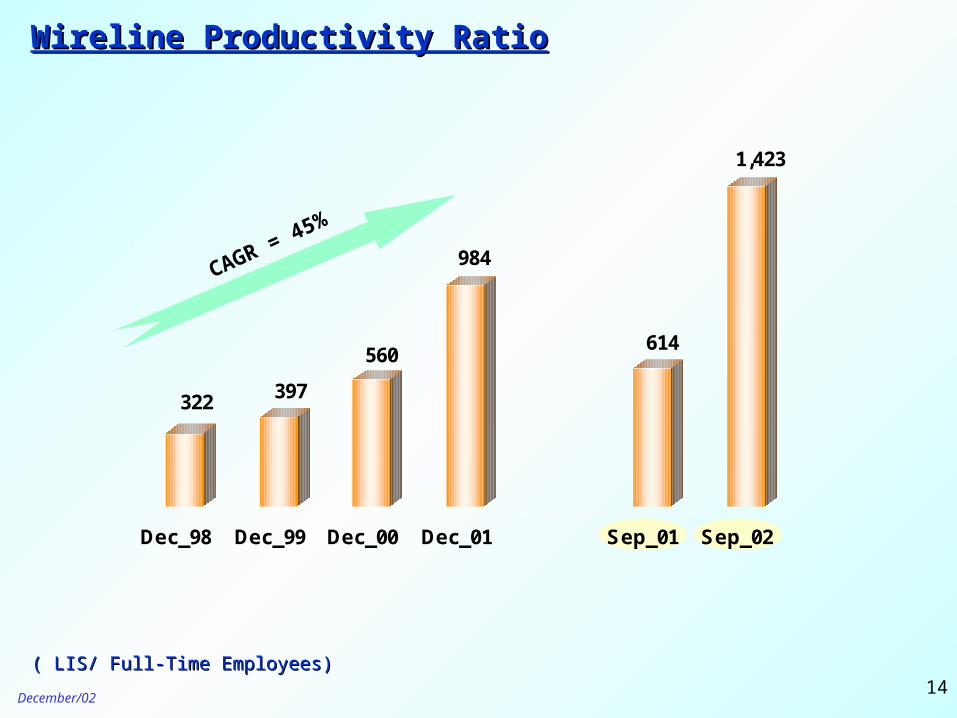

322 397

560

984

614

1,423

Dec_98 Dec_99 Dec_00 Dec_01 Sep_01 Sep_02

Wireline Productivity RatioWireline Productivity Ratio

CAGR = 45%

( LIS/ Full-Time Employees)( LIS/ Full-Time Employees)

December/0215

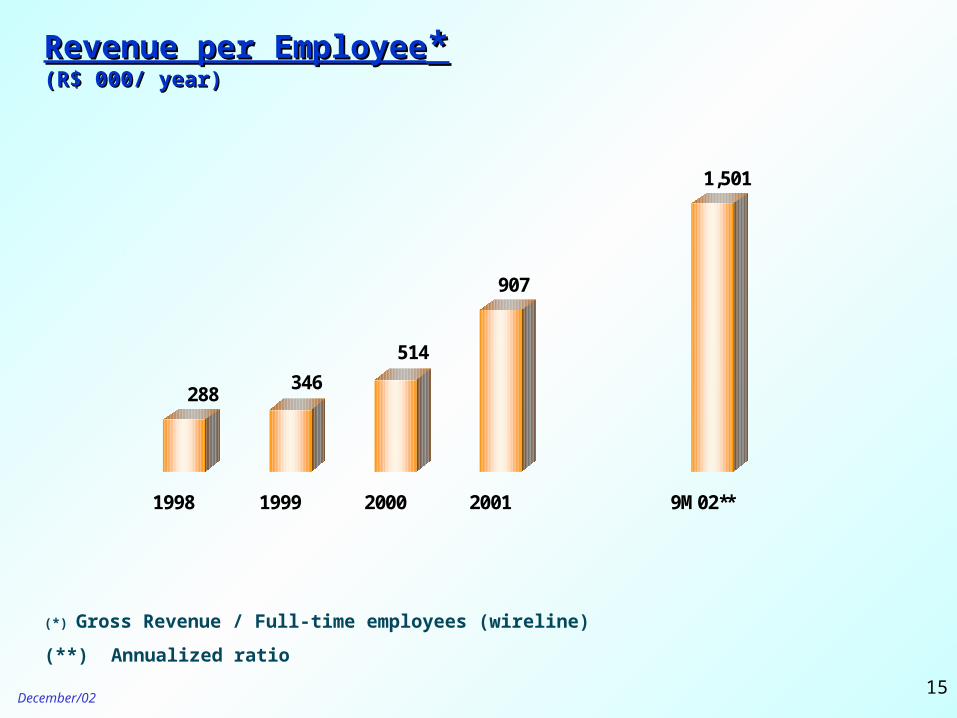

Revenue per EmployeeRevenue per Employee**(R$ 000/ year)(R$ 000/ year)

(*) Gross Revenue / Full-time employees (wireline)

(**) Annualized ratio

288346

514

907

1,501

1998 1999 2000 2001 9M02**

December/0216

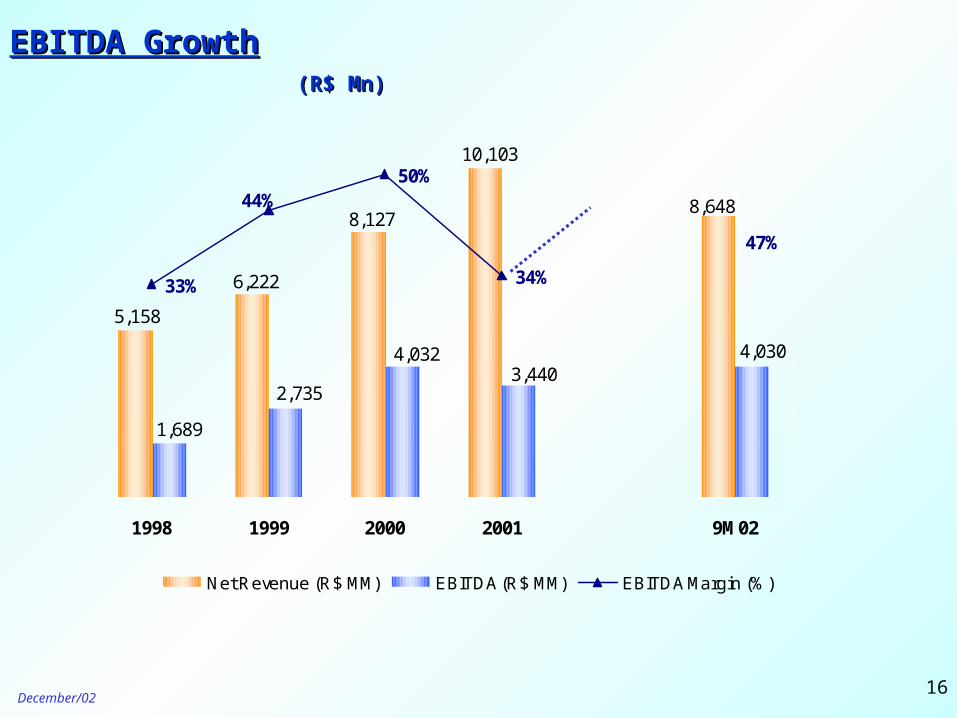

EBITDA GrowthEBITDA Growth (R$ Mn)(R$ Mn)

8,6488,127

6,222

10,103

5,158

4,030

1,689

2,735

4,0323,440

33%

50%

34%

47%

44%

1998 1999 2000 2001 9M02

Net Revenue (R$ MM) EBITDA (R$ MM) EBITDA Margin (%)

December/0217

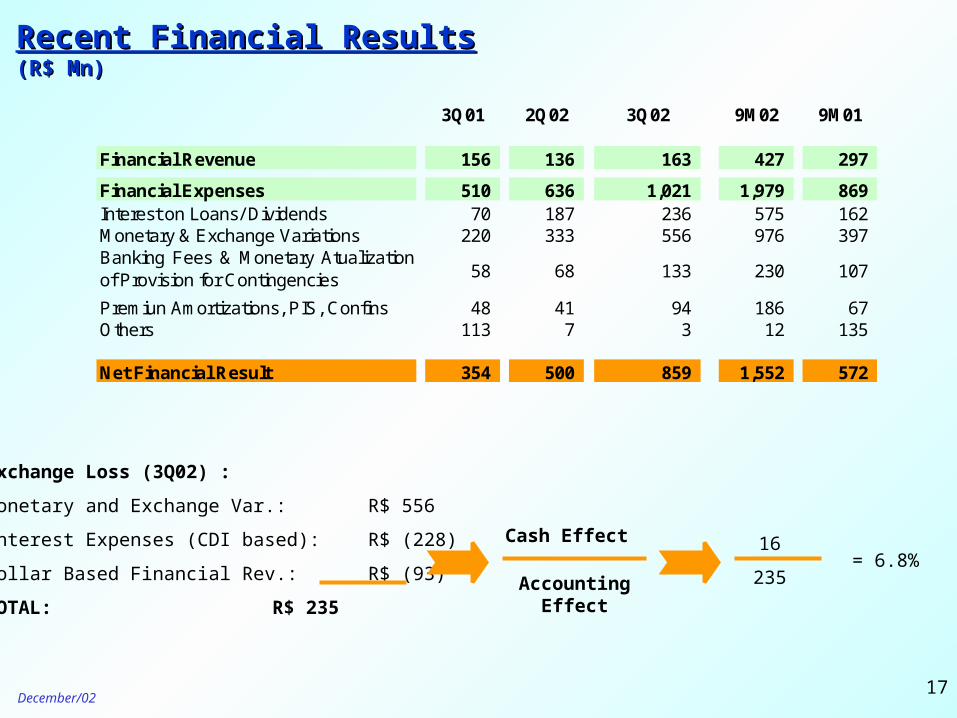

Recent Financial ResultsRecent Financial Results(R$ Mn)(R$ Mn)

Exchange Loss (3Q02) :

Monetary and Exchange Var.: R$ 556

Interest Expenses (CDI based): R$ (228)

Dollar Based Financial Rev.: R$ (93)

TOTAL: R$ 235

16

235= 6.8%

Cash Effect

Accounting Effect

3Q01 2Q02 3Q02 9M02 9M01

Financial Revenue 156 136 163 427 297

Financial Expenses 510 636 1,021 1,979 869 Interest on Loans/ Dividends 70 187 236 575 162 Monetary & Exchange Variations 220 333 556 976 397

Premiun Amortizations, PIS, Confins 48 41 94 186 67 Others 113 7 3 12 135

Net Financial Result 354 500 859 1,552 572

230 107 Banking Fees & Monetary Atualizationof Provision for Contingencies 133 68 58

December/0218

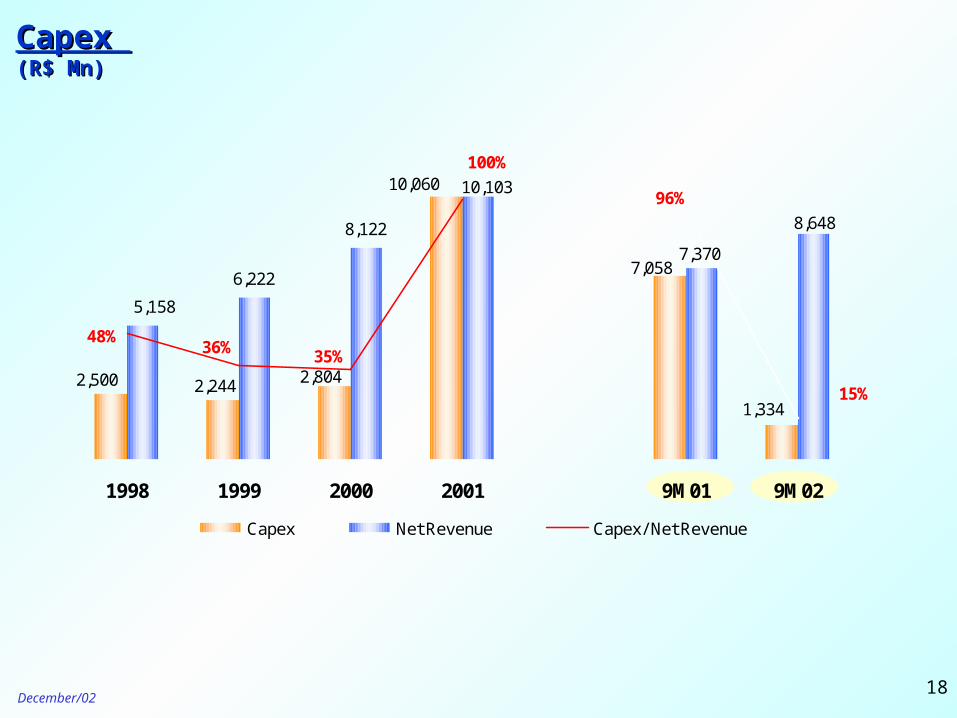

6,222

8,122

2,500 2,244 2,804

7,058

1,334

10,060 10,103

5,158

7,370

8,648

48%36% 35%

100%

96%

15%

1998 1999 2000 2001 9M01 9M02

Capex Net Revenue Capex/ Net Revenue

Capex Capex (R$ Mn)(R$ Mn)

December/0219

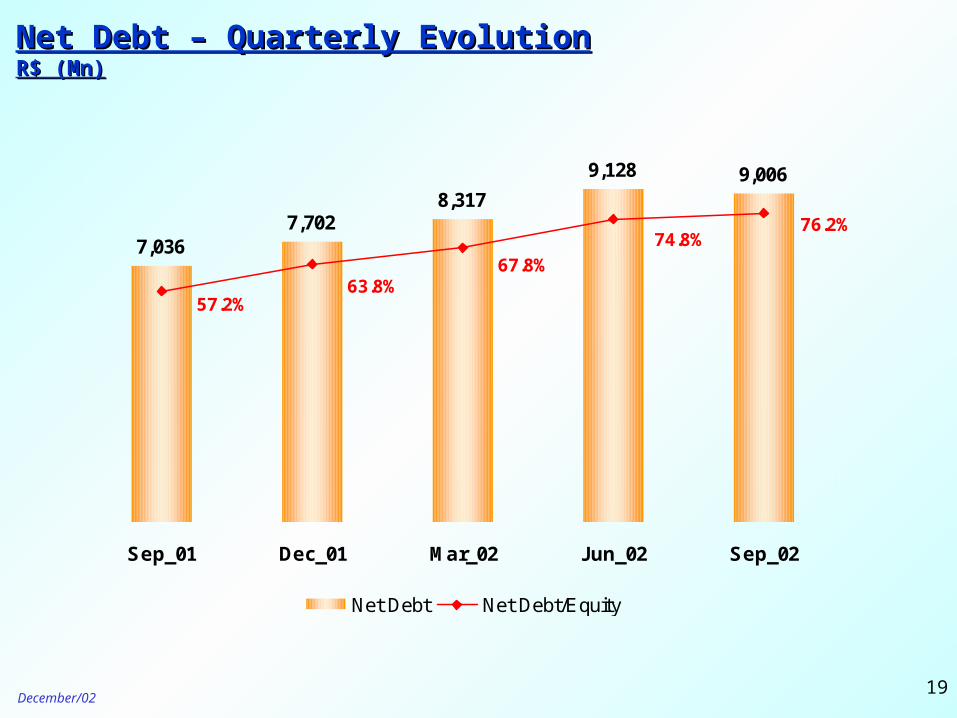

Net Debt – Quarterly EvolutionNet Debt – Quarterly EvolutionR$ (Mn)R$ (Mn)

7,0367,702

8,317

9,128 9,006

67.8%63.8%

74.8%

57.2%

76.2%

Sep_01 Dec_01 Mar_02 Jun_02 Sep_02

Net Debt Net Debt/Equity

December/0220

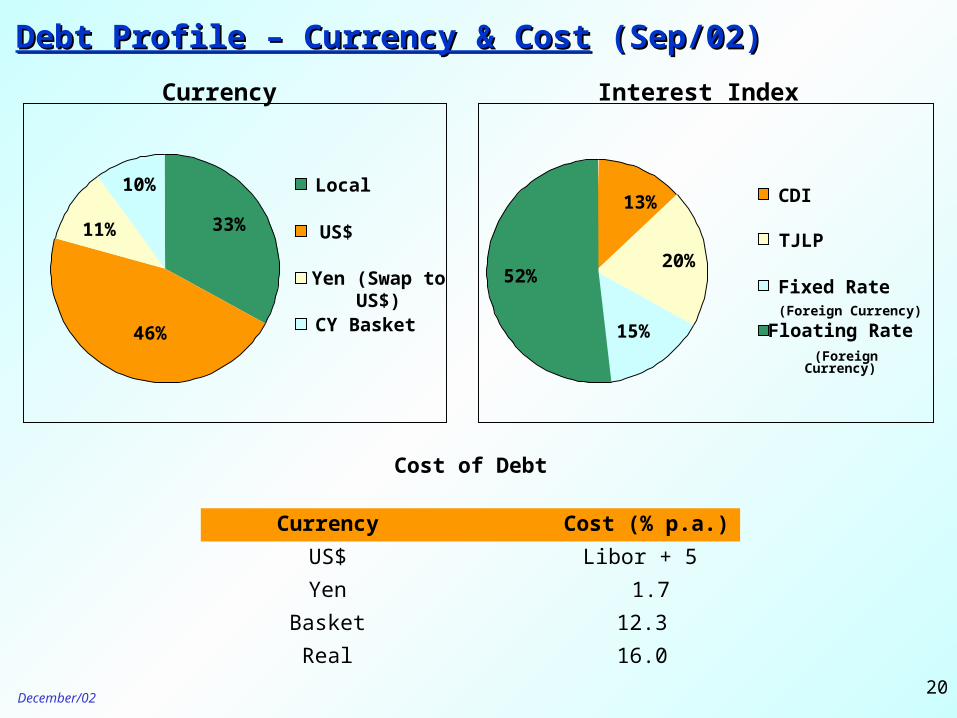

Debt Profile – Currency & CostDebt Profile – Currency & Cost (Sep/02) (Sep/02)

Currency

46%

11%

10%

33%

Local

US$

Yen (Swap to US$)

CY Basket

52%

15%

20%

13% CDI

TJLP

Fixed Rate (Foreign Currency)

Floating Rate (Foreign Currency)

Interest Index

Currency Cost (% p.a.)

US$ Libor + 5

Yen 1.7

Basket 12.3

Real 16.0

Cost of Debt

December/0221

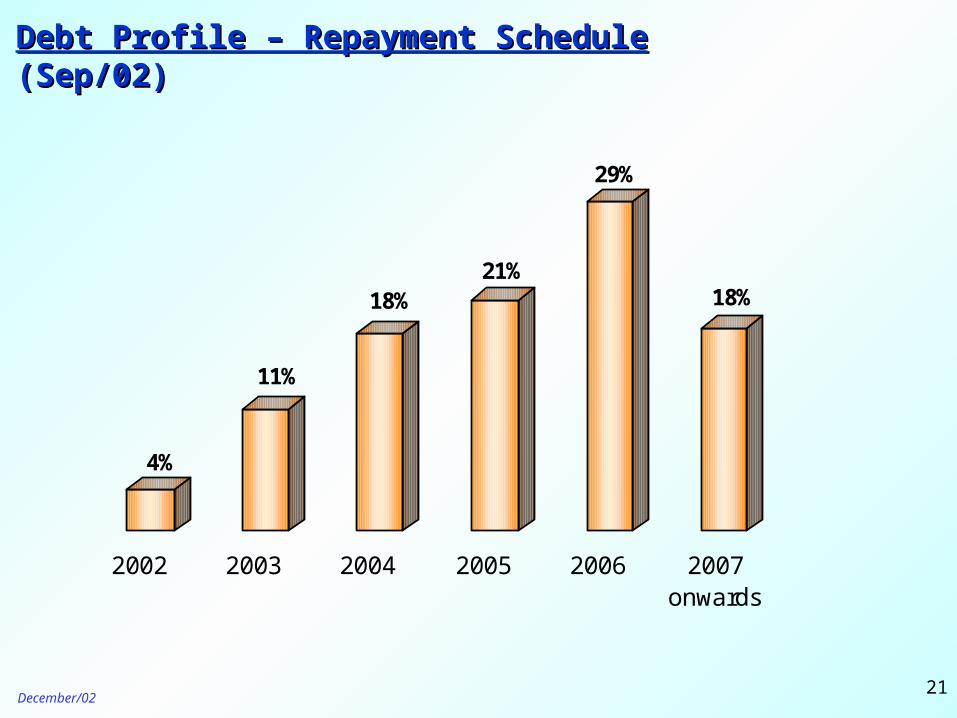

Debt Profile – Repayment ScheduleDebt Profile – Repayment Schedule (Sep/02) (Sep/02)

4%

11%

18%21%

29%

18%

2002 2003 2004 2005 2006 2007onwards

December/0222

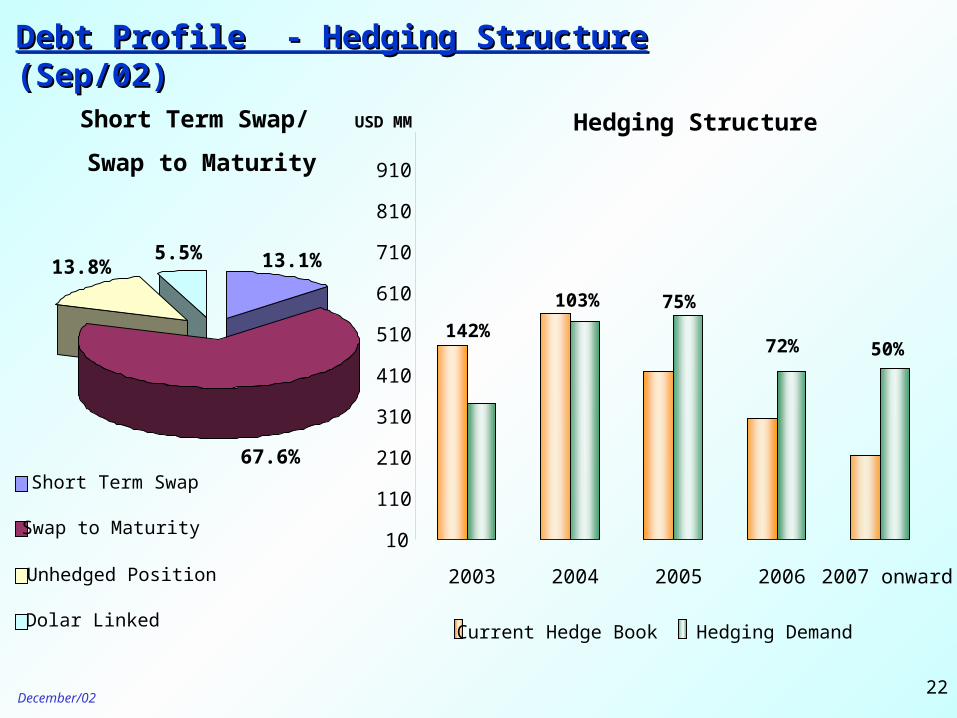

Debt Profile - Hedging StructureDebt Profile - Hedging Structure (Sep/02) (Sep/02)

Short Term Swap/

Swap to Maturity

USD MM

67.6%

13.1%13.8%5.5%

Short Term Swap

Swap to Maturity

Unhedged Position

Dolar Linked

142%

103% 75%

72% 50%

10

110

210

310

410

510

610

710

810

910

2003 2004 2005 2006 2007 onward

Current Hedge Book Hedging Demand

Hedging Structure

December/0223

978,000 subscribers in only 6 months of operations (Nov/02);

R$ 36.00 ARPU in the 3Q02;

78% pre and 22% post paid clients;

Financing US$ 1.4 billion credit (suppliers and bank facilities);

Coverage: 14 states – 396 cities;

2,360 integrated sites;

GSM National and International roaming (23 countries);

Net Revenue in 9 months: R$ 152 million;

Total debt in Sep/02: R$ 3.9 billion;

Network CAPEX through 2004: R$ 2.7 billion (R$ 1.8 billion until Sep/02).

TNE – PCS ´´Oi´´ - Current StatusTNE – PCS ´´Oi´´ - Current Status

December/0224

OUTLOOK 2002OUTLOOK 2002

Lines in Service: +400 K in 2002

Revenue: New DLD/ILD services and Oi (PCS)

Capex/02: up to R$ 2 bn

Bad Debt: up to 5% of Gross Revenue

Net Debt: around R$ 9bn (2002 YE)

Oi: 1 mn subscribers (2002 YE)

December/0225

This presentation contains forward-looking statements. Statements that are not historical facts,

including statements about our beliefs and expectations, are forward-looking statements and involve

inherent risks and uncertainties. These statements are based on current plans, estimates and

projections, and therefore you should not place undue reliance on them. Forward-looking statements

speak only as of the date they are made, and we undertake no obligation to update publicly any of them

in light of new information or future events.

““SAFE HARBOR” STATEMENTSAFE HARBOR” STATEMENT

Investor Relations

Rua Humberto de Campos, 425 / 8º andar

Leblon

Rio de Janeiro -RJ

Phone: ( 55 21) 3131-1314/1313/1315/1316/1317

Fax: (55 21) 3131-1155

E-mail: [email protected]

Visit our website: http://www.telemar.com.br/ri