Systemic risk, stress testing and financial …...Maximum entropy assumption. Individual...

37

BIS CCA-006-2010 May 2010 Systemic risk, stress testing and financial contagion: Their interaction and measurement A presentation prepared for the BIS CCA Conference on “Systemic risk, bank behaviour and regulation over the business cycle” Buenos Aires, 18–19 March 2010 Authors*: Serafín Martínez-Jaramillo, Calixto López Castañón, Omar Pérez Pérez, Fernando Avila Embriz and Fabrizio López Gallo Dey Affiliation: Bank of Mexico Email: [email protected] , [email protected] , [email protected] , [email protected] , [email protected] * This presentation reflects the views of the authors and not necessarily those of the BIS or of central banks participating in the meeting.

Transcript of Systemic risk, stress testing and financial …...Maximum entropy assumption. Individual...

BIS CCA-006-2010

May 2010

Systemic risk, stress testing and financial contagion: Their interaction and measurement

A presentation prepared for the BIS CCA Conference on

“Systemic risk, bank behaviour and regulation over the business cycle”

Buenos Aires, 18–19 March 2010

Authors*: Serafín Martínez-Jaramillo, Calixto López Castañón, Omar Pérez Pérez, Fernando Avila Embriz and Fabrizio López Gallo Dey

Affiliation: Bank of Mexico

Email: [email protected], [email protected], [email protected], [email protected], [email protected]

* This presentation reflects the views of the authors and not necessarily those of the BIS or of central banks

participating in the meeting.

MotivationThe Simulation Model and Results

Summary

Systemic Risk, Stress Testing and FinancialContagion: Their Interaction and Measurement

(Work in progress)

Serafín Martínez-Jaramillo1 Calixto López Castañón1

Fabrizio López Gallo Dey1 Omar Pérez Pérez1

Fernando Avila Embriz1

1Financial System Analysis DirectorateBanco de Mexico

Systemic risk, bank behaviour and regulation over thebusiness cycle, 2010

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Outline

1 MotivationRelevant ConceptsRelated Literature

2 The Simulation Model and ResultsThe Simulation ModelResults

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Outline

1 MotivationRelevant ConceptsRelated Literature

2 The Simulation Model and ResultsThe Simulation ModelResults

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Systemic RiskDefinition

Systemic Risk is the risk of experiencing an event thatthreatens the well functioning of the system of interest(payments, banking, financial).Systemic risk consists of two main components (Rochet2009, Marquez & Martinez-Jaramillo 2009):

An initial (macroeconomic) shock, andA contagion mechanism.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Stress Testing

From a financial authority point of view, the methodologies forthe design of stress tests can be divided in two approaches:

The bottom up approach and

The top down approach.

In this work we employ the bottom up approach as we possesrelatively good information on the individual banks and theinterbank market.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Financial Contagion

Financial contagion is one of the key elements on the definitionof systemic risk; in fact, both terms were used in aninterchangeable way in the past.It is necessary to distinguish between two different types ofcontagion:

Direct contagion has been studied widely by severalcentral banks.

Indirect contagion is difficult to estimate due to the inherentinformation problems.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Financial Contagion in the Mexican Banking System

Figure:Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Outline

1 MotivationRelevant ConceptsRelated Literature

2 The Simulation Model and ResultsThe Simulation ModelResults

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Financial Contagion.

Direct contagion in banking systems through the interbankmarket has been widely studied by central banks in severalcountries, Upper(2007).

Maximum entropy assumption.Individual idiosyncratic failures.

More recently contagion and systemic risk have beenstudied recurring to Network Theory, Muller (2006), Nier etal (2006), Babus (2007), Mistrulli (2007), Markose et al(2009).

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Stress Testing.

The proposed simulation model allows for coherentsystem-wide stress testing including second round effects,Cihak (2007).

The design of scenarios is a relevant aspect in stresstesting; in fact, the result of the stress tests dependsheavily on the design of such macroeconomic scenarios.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Relevant ConceptsRelated Literature

Systemic risk.

Goodhart et al. (2006) propose a general equilibriummodel which includes heterogeneous agents, endogenousdefaults and credit and deposit markets.

Segoviano and Goodhart (2009) infer the multivariatedensity, which they use to derive relevant measures ofdistress for individual banks, groups of banks and thedistress on the system due to an individual bank.

Boss et al. (2006) use a simulation model which they useto estimate the distribution of losses for the system as awhole.

Aikman et al. (2009) put in place a complex simulationmodel to study financial stability.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Outline

1 MotivationRelevant ConceptsRelated Literature

2 The Simulation Model and ResultsThe Simulation ModelResults

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

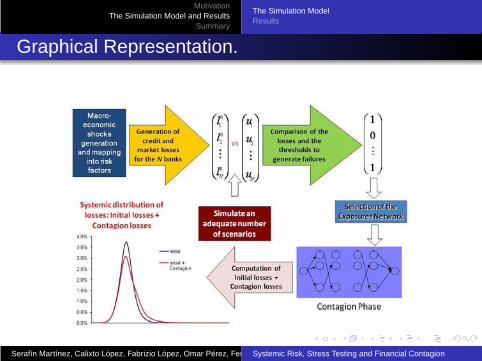

Graphical Representation.

Figure: The simulation algorithm.Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Data

The data used to obtain the systemic distribution of losses forthe Mexican banking system consists of:

The daily interbank exposures,

The macro economic information used to build the macromodels (GDP, interest rates, stock indexes, etc),

The market portfolio and

Credit delinquency ratio as a proxy for the evolution ofcredit losses.

The Tier 1 capital.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

The Link to the Economic Variables.

Previous versions of this work, Marquez &Martinez-Jaramillo (2009), computed the joint distributionof losses from market and credit operations, and thisdistribution was used to generate “losses draws” and todetermine whether those losses trigger a contagionprocess.

Despite the advantages of this method, behind each shockwas the idea that “something happened” but there was fewto say about what that “something” was.

Hence, to gain in the interpretation and to ease the stresstesting procedure one of the aims is having scenarios withan economic interpretation.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

The Link to the Economic Variables II.

To generate these scenarios linked to real economicvariables within a consistent framework, a simple structuralVAR was estimated:

Yt =

p∑

i=1

AiYt−i +12∑

m=1

δmDmt + et . (1)

The variables used are: (all expressed in differences inlogs) IGAE, General Economic Activity Index. (y), which isa close indicator of GDP, Cete interest rate (r c), theconsumer price index (π), exchange rate (e), the Mexicanstock exchange index (ipc), the delinquency rate in bankloans (DR), treasury bill interest rate (r tb), libor interest rate(rL), the Dow Jones stock index (DJ), and the Brazilianstock index Bovespa.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

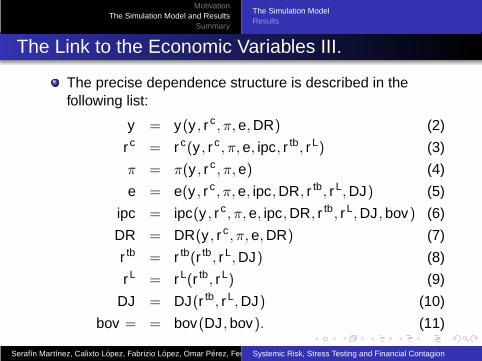

The Link to the Economic Variables III.

The precise dependence structure is described in thefollowing list:

y = y(y , r c , π, e, DR) (2)

r c = r c(y , r c , π, e, ipc, r tb, rL) (3)

π = π(y , r c , π, e) (4)

e = e(y , r c , π, e, ipc, DR, r tb, rL, DJ) (5)

ipc = ipc(y , r c , π, e, ipc, DR, r tb, rL, DJ, bov) (6)

DR = DR(y , r c , π, e, DR) (7)

r tb = r tb(r tb, rL, DJ) (8)

rL = rL(r tb, rL) (9)

DJ = DJ(r tb, rL, DJ) (10)

bov = = bov(DJ, bov). (11)

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

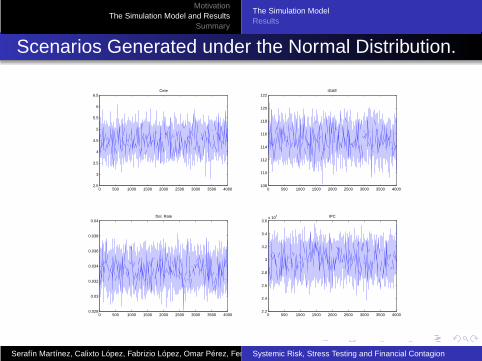

Scenarios Generated under the Normal Distribution.

0 500 1000 1500 2000 2500 3000 3500 40002.5

3

3.5

4

4.5

5

5.5

6

6.5Cete

0 500 1000 1500 2000 2500 3000 3500 4000108

110

112

114

116

118

120

122IGAE

0 500 1000 1500 2000 2500 3000 3500 40000.028

0.03

0.032

0.034

0.036

0.038

0.04Del. Rate

0 500 1000 1500 2000 2500 3000 3500 40002.2

2.4

2.6

2.8

3

3.2

3.4

3.6x 10

4 IPC

Figure:Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Outline

1 MotivationRelevant ConceptsRelated Literature

2 The Simulation Model and ResultsThe Simulation ModelResults

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

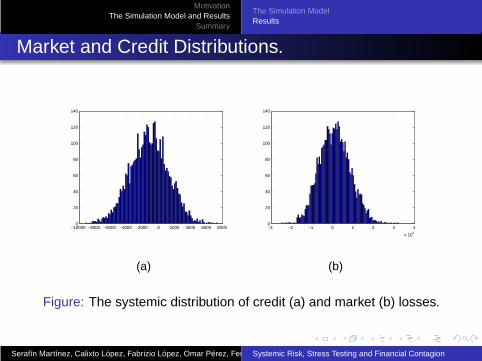

Market and Credit Distributions.

−10000 −8000 −6000 −4000 −2000 0 2000 4000 6000 80000

20

40

60

80

100

120

140

(a)

−3 −2 −1 0 1 2 3 4

x 104

0

20

40

60

80

100

120

140

(b)

Figure: The systemic distribution of credit (a) and market (b) losses.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Joint Distribution.

−3 −2 −1 0 1 2 3 4

x 104

0

20

40

60

80

100

120

140

Figure: The systemic distribution of losses for the Mexican bankingsystem.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Systemic Relevance of an Institution.

There are recent attempts to measure the systemic relevanceof a financial institution. For example:

Based on the Shapley value (Borio et al 2009).

Based on several measures like size, interconnectedness,lack of substitutability (BIS, FSB and IMF)

Based on the CoVaR(Adrian et al 2009)

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

CoVaR definition(Adrian et al 2009).

Institution i ’s CoVaR relative to an institution j (the system) isdefined as the VaR of the institution j (or the whole financialsector) conditional on institution i being in distress.

Pr(X j ≤ CoVaR j|iq | X i = VaR i

q) = q.

The difference between the CoVaR and the unconditionalfinancial system VaR, ∆CoVaR, captures the marginalcontribution of a particular institution to the overall systemicrisk.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

CoVaR example.

−4 −3 −2 −1 0 1 2 3 4

x 104

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

SystemSystem given B1System given B2System given B3System given B4System given B5System given B6System given B7

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Systemic events.

Contagion did not happen under the previous 20ksimulations.

Contagion did happen under Montecarlo simulation (5m).

Systemic events are located on the tail.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

“Tail Scenarios”

0 200 400 600 800 10003

3.5

4

4.5

5

5.5

6

6.5

7

7.5

8Cete

0 200 400 600 800 1000102

104

106

108

110

112

114

116

118

120

122IGAE

0 200 400 600 800 10000.028

0.03

0.032

0.034

0.036

0.038

0.04

0.042

0.044

0.046Del. Rate

0 200 400 600 800 10001

1.5

2

2.5

3

3.5

4x 10

4 IPC

Figure:Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Tail Market and Credit Distributions.

−2 −1.5 −1 −0.5 0 0.5 1

x 104

0

50

100

150

200

250

(a)

−5 −4 −3 −2 −1 0 1 2 3 4

x 104

0

50

100

150

200

250

(b)

Figure: The systemic distribution of credit (a) and market (b) losses5000 scenarios including 1000 biased scenarios on the tail.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Joint Tail Distribution.

−6 −4 −2 0 2 4

x 104

0

50

100

150

200

250

Figure: The systemic distribution of losses for the Mexican bankingsystem 5000 scenarios including 1000 biased scenarios.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

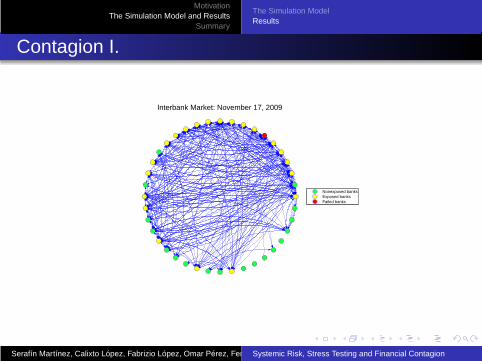

Contagion I.

Interbank Market: November 17, 2009

Nonexposed banksExposed banksFailed banks

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

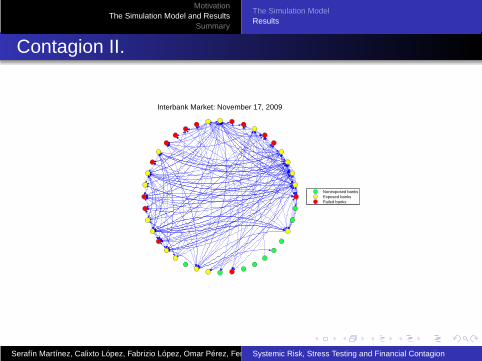

Contagion II.

Interbank Market: November 17, 2009

Nonexposed banksExposed banksFailed banks

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

Contagion III.

Interbank Market: November 17, 2009

Nonexposed banksExposed banksFailed banks

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

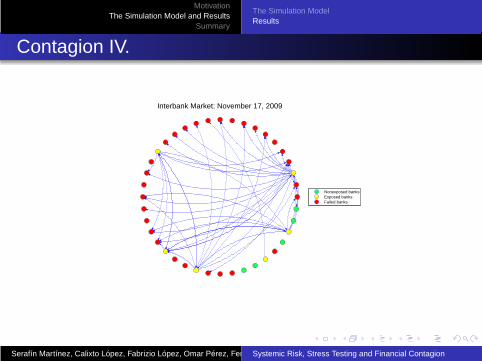

Contagion IV.

Interbank Market: November 17, 2009

Nonexposed banksExposed banksFailed banks

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

The Simulation ModelResults

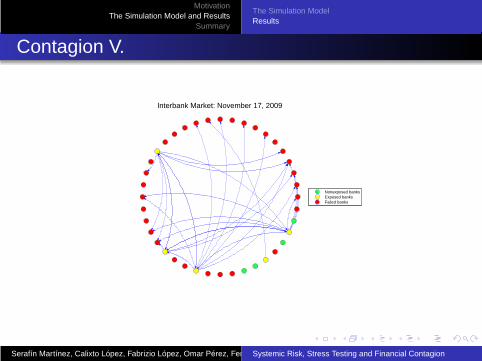

Contagion V.

Interbank Market: November 17, 2009

Nonexposed banksExposed banksFailed banks

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Summary

The literature adhered to the belief that the topology of thenetwork was enough to characterize the systemic riskinessof a particular financial system.The relevance of the initial macroeconomic shock shouldnot be disregarded.Finally, to concentrate on size and interconnectedness todetermine the systemic importance of institutions could bemisleading.

Future work:The issue here is how to deal with the implicit trade-off: amore accurate credit risk measurement requires a sacrificein the market risk measurement accuracy and viceversa.Using a distribution with heavier tails is an alternative worthexploring that wouldn’t require a change of paradigm.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Thanks

Thank you!

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion

MotivationThe Simulation Model and Results

Summary

Questions

Questions.

Serafín Martínez, Calixto López, Fabrizio López, Omar Pérez, Fernando AvilaSystemic Risk, Stress Testing and Financial Contagion