Aula Abertura AnoLetivo - fep.up.pt _AnoLetivo... ·...

29

20 de Outubro de 2011 Fernando Teixeira dos Santos 20 de Outubro de 2011 Fernando Teixeira dos Santos 20 de Outubro de 2011 20 de Outubro de 2011 Fernando Teixeira dos Santos 20 de Outubro de 2011 No verão de 2007, estavamos longe de imaginar o que nos esperava. Esta é a história da metamorfose de uma crise que começou por ser crise de crédito imobiliário e que passou a crise financeira e bancária, depois a crise económica, a crise orçamental/dívida soberana, a crise do euro, novamente uma crise bancária e poderá vir a ser mais uma vez uma crise económica e eventualmente uma crise políEca da UE. Uma crise em que Everam que ser tomadas decisões na base de informação limitada e num contexto de elevada incerteza. Uma crise com altos e baixos pois houve períodos em que pareceu que as dificuldades estavam a ser ultrapassadas. Infelizmente, períodos que se revelaram efémeros, retomando a crise novas facetas cada vez mais gravosas.

-

Upload

dinhkhuong -

Category

Documents

-

view

215 -

download

0

Transcript of Aula Abertura AnoLetivo - fep.up.pt _AnoLetivo... ·...

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

#

Fernando#Teixeira#dos#Santos#############################20#de#Outubro#de#2011##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

No#verão#de#2007,#estavamos#longe#de#imaginar#o#que#nos#esperava.#Esta#é#a#história#da#metamorfose#de#uma#crise#que#começou#por#ser#crise#de#crédito#imobiliário#e#que##passou#a#crise#financeira#e#bancária,#depois#a#crise#económica,#a#crise#orçamental/dívida#soberana,#a#crise#do#euro,#novamente#uma#crise#bancária#e#poderá#vir#a#ser#mais#uma#vez##uma#crise#económica#e#eventualmente#uma#crise#políEca#da#UE.#Uma#crise#em#que#Everam#que#ser#tomadas#decisões#na#base#de#informação#limitada#e#num#contexto#de#elevada#incerteza.##Uma#crise#com#altos#e#baixos#pois#houve#períodos#em#que#pareceu#que#as#dificuldades#estavam#a#ser#ultrapassadas.#Infelizmente,#períodos#que#se#revelaram#efémeros,#retomando#a#crise#novas#facetas#cada#vez#mais#gravosas.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

1. Breve#caracterização#da#crise#atual#2. Origens#e#desenvolvimento:#do#subprime)à#

crise#das#dívidas#soberanas##3. Fragilidades#e#desafios#dos#“soberanos”:#a#

crise#do#euro#4. Impacto#da#crise#do#euro#no#setor#financeiro#5. A#saída#da#crise#6. Conclusão:#Portugal#e#a#crise#do#euro#

#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

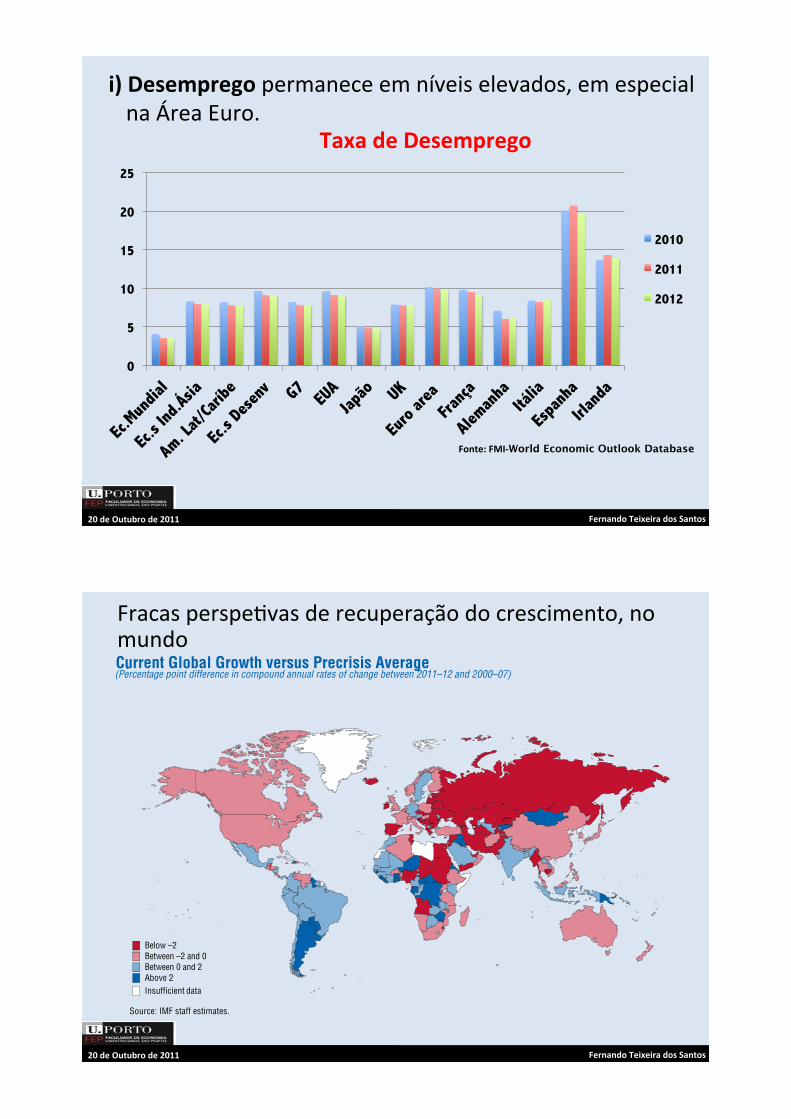

i)#Desemprego#permanece#em#níveis#elevados,#em#especial#na#Área#Euro.#

#

Taxa#de#Desemprego#

Fonte:#FMI?World Economic Outlook Database#

0

5

10

15

20

25

2010

2011

2012

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

International Monetary Fund | September 2011 71

The global economy has slowed, financial volatility and investor risk aversion have sharply increased, and perfor-mance has continued to diverge across regions (Figure 2.1). In the United States, weak growth and the lack of a cred-ible medium-term fiscal plan to reduce debt are draining confidence. Europe is gripped with financial strains from the sovereign debt crisis in the euro area periphery. How these advanced economies confront their fiscal challenges will profoundly affect their economic prospects. Emerging and developing economies as a group continue to expand, a few at rates well above their precrisis averages. However, growth will likely moderate as the slowdown in major advanced economies weighs on external demand. Finally, inflation remains elevated (Figure 2.2). Although this is explained mainly by resurgent commodity prices in the first half of the year, in some economies, demand pressures—stoked by accommodative policies, strong credit growth, and capital

inflows—have contributed as well. Policy tightening, to eliminate inflation pressure and strengthen fiscal accounts, is essential to sustain balanced growth in these economies. Where overheating and fiscal risks are not imminent, further tightening can wait until risks to global stability subside.

Almost three years after the crisis, the global economy continues to be challenged with intermit-tent volatility. Economic performance has become even more bipolar in nature, with anemic growth in economies with large precrisis imbalances and robust activity in many others. As discussed earlier, the unbalanced expansion re!ects an inadequate transi-tion from public to private demand in advanced economies and from external-demand-driven growth to domestic-demand-driven growth in key emerg-ing and developing economies. Without progress on

Below –2Between –2 and 0Between 0 and 2Above 2Insufficient data

Figure 2.1. Current Global Growth versus Precrisis Average (Percentage point difference in compound annual rates of change between 2011–12 and 2000–07)

Source: IMF staff estimates.Note: There are no data for Libya in the projection years due to the uncertain political situation. Projections for 2011 and later exclude South Sudan. Due to data limitations, data for Iraq are the growth differential between the average in 2011–12 and 2005–07; for Afghanistan between the average in 2011–12 and 2003–07; and for Kosovo, Liberia, Malta, Montenegro, Tuvalu, and Zimbabwe between the average in 2011–12 and 2001–07.

2CHAPTER COUNTRY AND REGIONAL PERSPECTIVES

International Monetary Fund | September 2011 71

The global economy has slowed, financial volatility and investor risk aversion have sharply increased, and perfor-mance has continued to diverge across regions (Figure 2.1). In the United States, weak growth and the lack of a cred-ible medium-term fiscal plan to reduce debt are draining confidence. Europe is gripped with financial strains from the sovereign debt crisis in the euro area periphery. How these advanced economies confront their fiscal challenges will profoundly affect their economic prospects. Emerging and developing economies as a group continue to expand, a few at rates well above their precrisis averages. However, growth will likely moderate as the slowdown in major advanced economies weighs on external demand. Finally, inflation remains elevated (Figure 2.2). Although this is explained mainly by resurgent commodity prices in the first half of the year, in some economies, demand pressures—stoked by accommodative policies, strong credit growth, and capital

inflows—have contributed as well. Policy tightening, to eliminate inflation pressure and strengthen fiscal accounts, is essential to sustain balanced growth in these economies. Where overheating and fiscal risks are not imminent, further tightening can wait until risks to global stability subside.

Almost three years after the crisis, the global economy continues to be challenged with intermit-tent volatility. Economic performance has become even more bipolar in nature, with anemic growth in economies with large precrisis imbalances and robust activity in many others. As discussed earlier, the unbalanced expansion re!ects an inadequate transi-tion from public to private demand in advanced economies and from external-demand-driven growth to domestic-demand-driven growth in key emerg-ing and developing economies. Without progress on

Below –2Between –2 and 0Between 0 and 2Above 2Insufficient data

Figure 2.1. Current Global Growth versus Precrisis Average (Percentage point difference in compound annual rates of change between 2011–12 and 2000–07)

Source: IMF staff estimates.Note: There are no data for Libya in the projection years due to the uncertain political situation. Projections for 2011 and later exclude South Sudan. Due to data limitations, data for Iraq are the growth differential between the average in 2011–12 and 2005–07; for Afghanistan between the average in 2011–12 and 2003–07; and for Kosovo, Liberia, Malta, Montenegro, Tuvalu, and Zimbabwe between the average in 2011–12 and 2001–07.

2CHAPTER COUNTRY AND REGIONAL PERSPECTIVES

International Monetary Fund | September 2011 71

The global economy has slowed, financial volatility and investor risk aversion have sharply increased, and perfor-mance has continued to diverge across regions (Figure 2.1). In the United States, weak growth and the lack of a cred-ible medium-term fiscal plan to reduce debt are draining confidence. Europe is gripped with financial strains from the sovereign debt crisis in the euro area periphery. How these advanced economies confront their fiscal challenges will profoundly affect their economic prospects. Emerging and developing economies as a group continue to expand, a few at rates well above their precrisis averages. However, growth will likely moderate as the slowdown in major advanced economies weighs on external demand. Finally, inflation remains elevated (Figure 2.2). Although this is explained mainly by resurgent commodity prices in the first half of the year, in some economies, demand pressures—stoked by accommodative policies, strong credit growth, and capital

inflows—have contributed as well. Policy tightening, to eliminate inflation pressure and strengthen fiscal accounts, is essential to sustain balanced growth in these economies. Where overheating and fiscal risks are not imminent, further tightening can wait until risks to global stability subside.

Almost three years after the crisis, the global economy continues to be challenged with intermit-tent volatility. Economic performance has become even more bipolar in nature, with anemic growth in economies with large precrisis imbalances and robust activity in many others. As discussed earlier, the unbalanced expansion re!ects an inadequate transi-tion from public to private demand in advanced economies and from external-demand-driven growth to domestic-demand-driven growth in key emerg-ing and developing economies. Without progress on

Below –2Between –2 and 0Between 0 and 2Above 2Insufficient data

Figure 2.1. Current Global Growth versus Precrisis Average (Percentage point difference in compound annual rates of change between 2011–12 and 2000–07)

Source: IMF staff estimates.Note: There are no data for Libya in the projection years due to the uncertain political situation. Projections for 2011 and later exclude South Sudan. Due to data limitations, data for Iraq are the growth differential between the average in 2011–12 and 2005–07; for Afghanistan between the average in 2011–12 and 2003–07; and for Kosovo, Liberia, Malta, Montenegro, Tuvalu, and Zimbabwe between the average in 2011–12 and 2001–07.

2CHAPTER COUNTRY AND REGIONAL PERSPECTIVES

Fracas#perspeEvas#de#recuperação#do#crescimento,#no#mundo##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

C H A P T E R 2 CO U N T RY A N D R E G I O N A L P E R S P E C T I V E S

International Monetary Fund | September 2011 77

contain the crisis in the euro area periphery, consis-tent with their commitments at the July EU summit. In the CEE economies, growth will slow from 4¼ percent in 2011 to about 2¾ percent in 2012, as both domestic and external demand moderate.

Economic performance will vary widely across Europe: • A few economies are operating close to average

precrisis rates, with little or no excess capacity (for example, Denmark, Germany, Netherlands, Poland, Sweden, Switzerland, Turkey), and in some cases unemployment rates are at or below typical precrisis levels. These economies avoided major precrisis imbalances and have benefited from the strong rebound in global manufactur-ing. Turkey, however, is experiencing a boom, driven to a large extent by overly accommodative policies.

• Some economies are noticeably below precrisis growth rates because of sharp economic adjustments in the context of financial crises. These include the euro area periphery countries that remain engulfed in deep sovereign debt crises (Greece, Ireland,

Portugal) with concurrent recessions or fragile growth. Others are recuperating from recent crises while addressing a number of challenges, including weak banking systems and/or high unemployment (Iceland, Latvia). These economies must steadfastly continue their balance sheet adjustment, which will likely keep output below capacity for some time.

• The rest of the region includes a wide spectrum of economies, most of which are likely to grow at less than precrisis averages. A few are shaken by contagion from the euro area periphery and are experiencing increasing market volatility and rising bond spreads (Italy, Spain), while others are less affected. Among the latter, some are projected to enjoy relatively solid growth (Bulgaria, Serbia); others continue to struggle (Croatia, United Kingdom). In#ation pressure is expected to stay well con-

tained, assuming receding commodity prices. In#a-tion in the euro area is expected to fall from 2½ percent in 2011 to about 1½ percent in 2012. In the CEE economies, the decline is expected to be from 5¼ percent in 2011 to 4½ percent in 2012.

Figure 2.5. Europe: Current Growth versus Precrisis Average(Percentage point difference in compound annual rates of changebetween 2011–12 and 2000–07)

Source: IMF staff estimates.Note: Due to data limitations, data for Kosovo, Malta, and Montenegro are the growth differential between the average in 2011–12 and in 2001–07.

Below –2Between –2 and 0Between 0 and 2Above 2

C H A P T E R 2 CO U N T RY A N D R E G I O N A L P E R S P E C T I V E S

International Monetary Fund | September 2011 77

contain the crisis in the euro area periphery, consis-tent with their commitments at the July EU summit. In the CEE economies, growth will slow from 4¼ percent in 2011 to about 2¾ percent in 2012, as both domestic and external demand moderate.

Economic performance will vary widely across Europe: • A few economies are operating close to average

precrisis rates, with little or no excess capacity (for example, Denmark, Germany, Netherlands, Poland, Sweden, Switzerland, Turkey), and in some cases unemployment rates are at or below typical precrisis levels. These economies avoided major precrisis imbalances and have benefited from the strong rebound in global manufactur-ing. Turkey, however, is experiencing a boom, driven to a large extent by overly accommodative policies.

• Some economies are noticeably below precrisis growth rates because of sharp economic adjustments in the context of financial crises. These include the euro area periphery countries that remain engulfed in deep sovereign debt crises (Greece, Ireland,

Portugal) with concurrent recessions or fragile growth. Others are recuperating from recent crises while addressing a number of challenges, including weak banking systems and/or high unemployment (Iceland, Latvia). These economies must steadfastly continue their balance sheet adjustment, which will likely keep output below capacity for some time.

• The rest of the region includes a wide spectrum of economies, most of which are likely to grow at less than precrisis averages. A few are shaken by contagion from the euro area periphery and are experiencing increasing market volatility and rising bond spreads (Italy, Spain), while others are less affected. Among the latter, some are projected to enjoy relatively solid growth (Bulgaria, Serbia); others continue to struggle (Croatia, United Kingdom). In#ation pressure is expected to stay well con-

tained, assuming receding commodity prices. In#a-tion in the euro area is expected to fall from 2½ percent in 2011 to about 1½ percent in 2012. In the CEE economies, the decline is expected to be from 5¼ percent in 2011 to 4½ percent in 2012.

Figure 2.5. Europe: Current Growth versus Precrisis Average(Percentage point difference in compound annual rates of changebetween 2011–12 and 2000–07)

Source: IMF staff estimates.Note: Due to data limitations, data for Kosovo, Malta, and Montenegro are the growth differential between the average in 2011–12 and in 2001–07.

Below –2Between –2 and 0Between 0 and 2Above 2

e#na#Europa##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

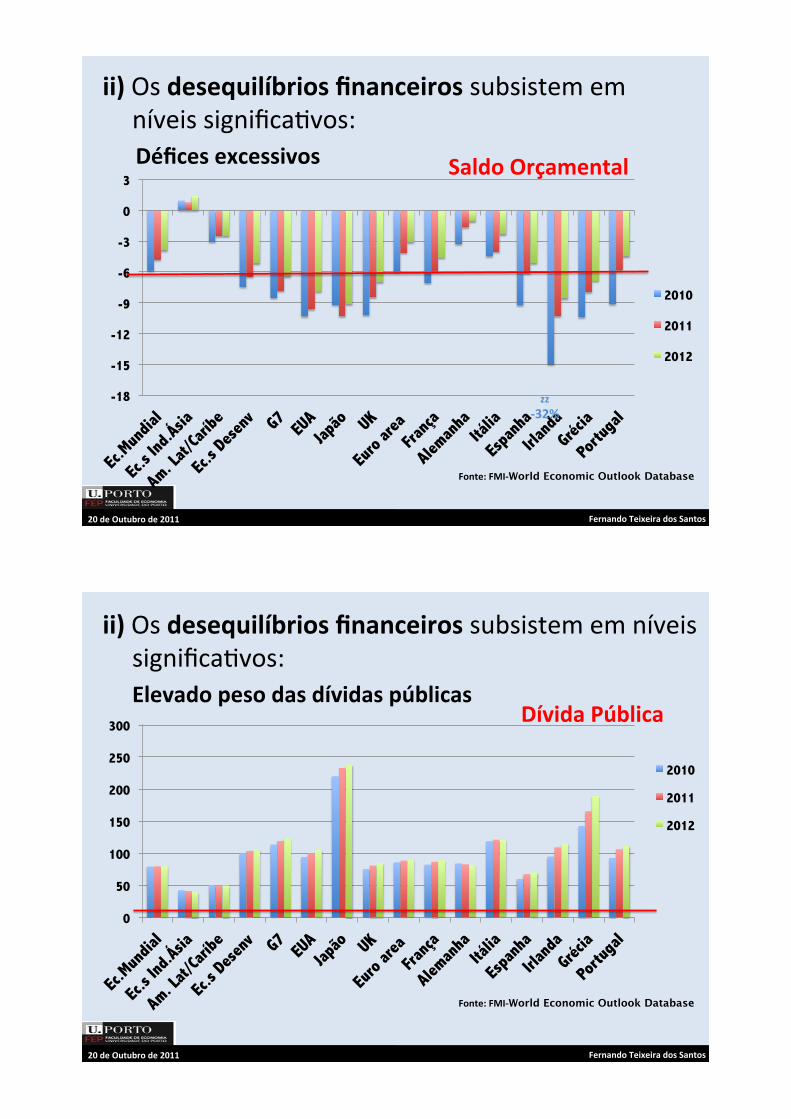

Espera[se#uma#desaceleração#do#crescimento#das#economias,#após#a#recuperação#de#2010.#

Taxa#de#Crescimento#

Fonte:#FMI?World Economic Outlook Database#

-6

-4

-2

0

2

4

6

8

10

2010

2011

2012

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

ii)#Os#desequilíbrios#financeiros#subsistem#em#níveis#significaEvos:##

######Défices#excessivos# Saldo#Orçamental#

Fonte:#FMI?World Economic Outlook Database#

-18

-15

-12

-9

-6

-3

0

3

2010

2011

2012

zz#

?32%#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

ii)#Os#desequilíbrios#financeiros#subsistem#em#níveis#significaEvos:#Elevado#peso#das#dívidas#públicas#

#Dívida#Pública#

Fonte:#FMI?World Economic Outlook Database#

0

50

100

150

200

250

300

2010

2011

2012

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Níveis#elevados#de#dívida#externa#na#generalidade#das#economias#mais#desenvolvidas#

Dívida#Externa#

Fonte: World Bank, World databank#

1100% xx

0%

100%

200%

300%

400%

500%

600%

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

com#ocorrência,#em#vários#países,#de#défices#significaEvos#da#balança#corrente#externa#refleEndo#problemas#de#compeEEvidade#externa#dessas#economias#e#de#insuficiência#de#poupança#interna.#

Saldo#Balança#Transações#Correntes#

Fonte:#FMI?World Economic Outlook Database#

-12 -10

-8 -6 -4 -2 0 2 4 6 8

2010

2011

2012

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

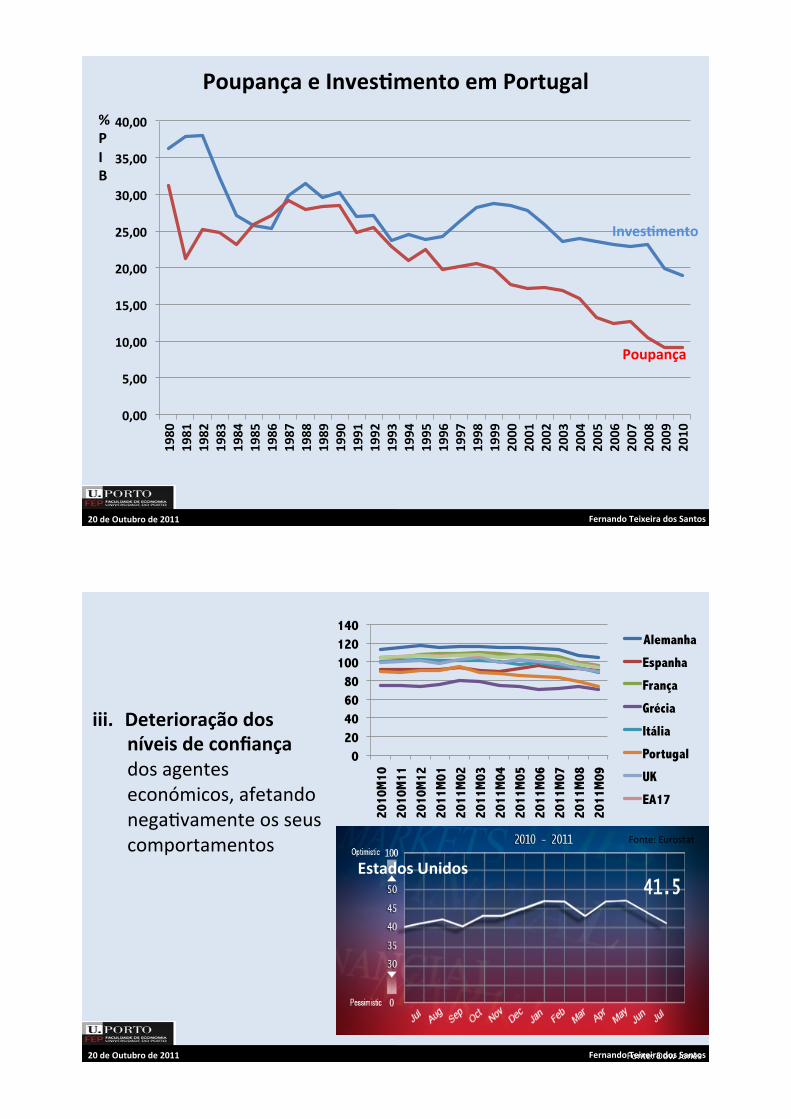

Poupança#e#InvesQmento#em#Portugal#

0,00#

5,00#

10,00#

15,00#

20,00#

25,00#

30,00#

35,00#

40,00#

1980#

1981#

1982#

1983#

1984#

1985#

1986#

1987#

1988#

1989#

1990#

1991#

1992#

1993#

1994#

1995#

1996#

1997#

1998#

1999#

2000#

2001#

2002#

2003#

2004#

2005#

2006#

2007#

2008#

2009#

2010#

%#

InvesQmento#

%#P#I#B#

Poupança#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

iii. Deterioração#dos#níveis#de#confiança#dos#agentes#económicos,#afetando#negaEvamente#os#seus#comportamentos#

0 20 40 60 80

100 120 140

2010

M10

20

10M

11

2010

M12

20

11M

01

2011

M02

20

11M

03

2011

M04

20

11M

05

2011

M06

20

11M

07

2011

M08

20

11M

09

Alemanha

Espanha

França

Grécia

Itália

Portugal

UK

EA17

Estados#Unidos#

Fonte:#Eurostat#

Fonte:#Dow#Jones#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

05/10/11#Moody's#rebaixa#a#Itália#e#o##Dexia#assombra#a#Europa#

07/10/11#A#Moody’s#anunciou#esta#manhã#um#corte##no#‘raQng’#de#seis#bancos#portugueses.#

14/09/11#Moody's#downgrades#Crédit#Agricole,#Société#Générale#

UK#Banks#downgraded#by#Moody's#raQng#agency######by#liamssog#|#October#7,#2011#at#02:55#am##on#Friday#7th#October#2011#Moody's#Investors#Service#downgrades#the#credit#raEng#of#12#UK#financial#firms#including#Lloyds#TSB,#RBS,#NaEonwide#and#Santander#UK.#

Moody's#downgrades#big#banks#on##changed#policy#

Sep#21,#2011#(Reuters)#[#Moody's#Investors#Service#lowered#debt#raEngs#for#Bank#of#America#Corp,#CiEgroup#Inc#and#Wells#Fargo#&#Co#on#Wednesday,#saying#the#U.S.#government#is#gerng#less#comfortable#with#bailing#out#large#troubled#lenders.#

iv. Spillovers#do#risco#soberano#sobre#o#sistema#bancário#fonte#de#dificuldades#com#retorno#sobre#os#próprios#soberanos.#

Eight#out#of#90#European#banks#have#failed#stress#tests#designed#to#ensure#they#can#withstand#another#financial#crisis.##

BUSINESS 15 July 2011 Last updated at 19:34 GMT

Eight banks fail EU stress test with 16 in danger zone

#######################

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

World Economic Outlook, September 2011

World Economic Outlook

Slowing Growth, Rising Risks

World Economic Outlook

Slowing Growth, Rising Risks

Wor ld Economic and F inancia l Surveys

I N T E R N A T I O N A L M O N E T A R Y F U N D

11SE

P

IMF

SEP

11

World Economic Outlook, September 2011

World Economic Outlook Slowing Growth, Rising Risks

World Economic Outlook

Slowing Growth, Rising Risks

Wor ld Economic and F inancia l Surveys

I N T E R N A T I O N A L M O N E T A R Y F U N D

11SE

P

IMF

SEP

11

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

i. Bom#desempenho#da#economia#mundial#nos#úlEmos#anos#e#disponibilidade#de#recursos#financeiros#avultados,#mas#com#fortes#desequílibrios#macroeconómicos#à#escala#global.#

ii. PolíEca#monetária#dos#Estados#Unidos#de#“easy-and-cheap-money”.#

iii. Deficiente#avaliação#do#risco.##iv. Inovação#financeira#e#proliferação#de#produtos#

financeiros#sintéEcos.##v. Regulação#e#supervisão#deficientes.##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

#• Assim#se#fizeram#hipotecas#de#alto#risco,#• a#parEr#das#quais,#graças#à#inovação#financeira,#se#criaram#produtos#financeiros#atraQvos#e#com#boa#notação#de#ra+ng,)

• produtos#transacionados#à#escala#global,#• intoxicando#progressiva#e#impercetvelmente#o#sistema#financeiro#internacional.#

#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

vi. Acumulação#de#incumprimentos#de#pagamento#dos#créditos#hipotecários#de#alto#risco#(subprime)#gerou#dificuldades#de#liquidez#e#perdas#com#efeitos#negaEvos#na#solvabilidade#das#insEtuições.#

#

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Trim.1_07 Trim.2_07 Trim.3_07 Trim.4_07 Trim.1_08 Trim.2_08 Trim.3_08

N°hipotecas#em#execução#?#EUA#

Fonte:#Foreclosure#Market#Report#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

vii. Redução#da#confiança#e#aumento#da#aversão#ao#risco.##Dificuldades#crescentes#na#obtenção#de#liquidez#afetando#mais#uns#bancos#que#outros#(flight)to)quality).#

Spread#face#aos#bunds-alemães#

Fonte:#ECB#StaQsQcal#Data#Warehouse#

0

20

40

60

80

100

120

2007

Jan

2007

Fev

2007

Mar

2007

Abr

2007

Mai

2007

Jun

2007

Jul

2007

Ago

2007

Set

2007

Out

2007

Nov

2007

Dez

2008

Jan

2008

Fev

2008

Mar

2008

Abr

2008

Mai

2008

Jun

2008

Jul

2008

Ago

2008

Set

2008

Out

BEL

ESP

FRA

GRE

IRL

ITA

PT

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

viii. A#falência#do#Lehman#Brothers#deu#uma#dimensão#claramente#sistémica#à#crise#do#subprime.#O#risco#de#colapso#do#sistema#financeiro#era#então#considerável.##

ix. A#quebra#de#confiança#dos#agentes#económicos,#as#restrições#de#crédito#provocadas#pela#crise#e#a#retração#do#comércio#internacional#Everam#efeitos#acentuados#na#aQvidade#económica#e#no#emprego#das#economias.###

Sofremos#assim#a#Grande#Recessão#de#2009.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

0,0 5,0

10,0 15,0 20,0 25,0

Ec.s

Des

env G7

Ec.in

d_As

ia

Outr

asEc

sDes

Euro

are

a

Fran

ça

Alem

anha

Sp

ain

Itál

ia

Gree

ce

Irel

and

Port

ugal

UK

US

A Ja

pan

2007 2010

Taxa#de#desemprego#

Crescimento#do#PIB#

-8,00 -6,00 -4,00 -2,00 0,00 2,00 4,00 6,00 8,00

Ec. M

undi

al

Ec.s

Des

env G7

Ec.in

d_As

ia

Outr

asEc

sDes

. Eu

ro a

rea

Fr

ance

Ge

rman

y Sp

ain

Ital

y Gr

eece

Ir

elan

d Po

rtug

al

Uk

USA

Japa

n

Média_05/07 2009

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

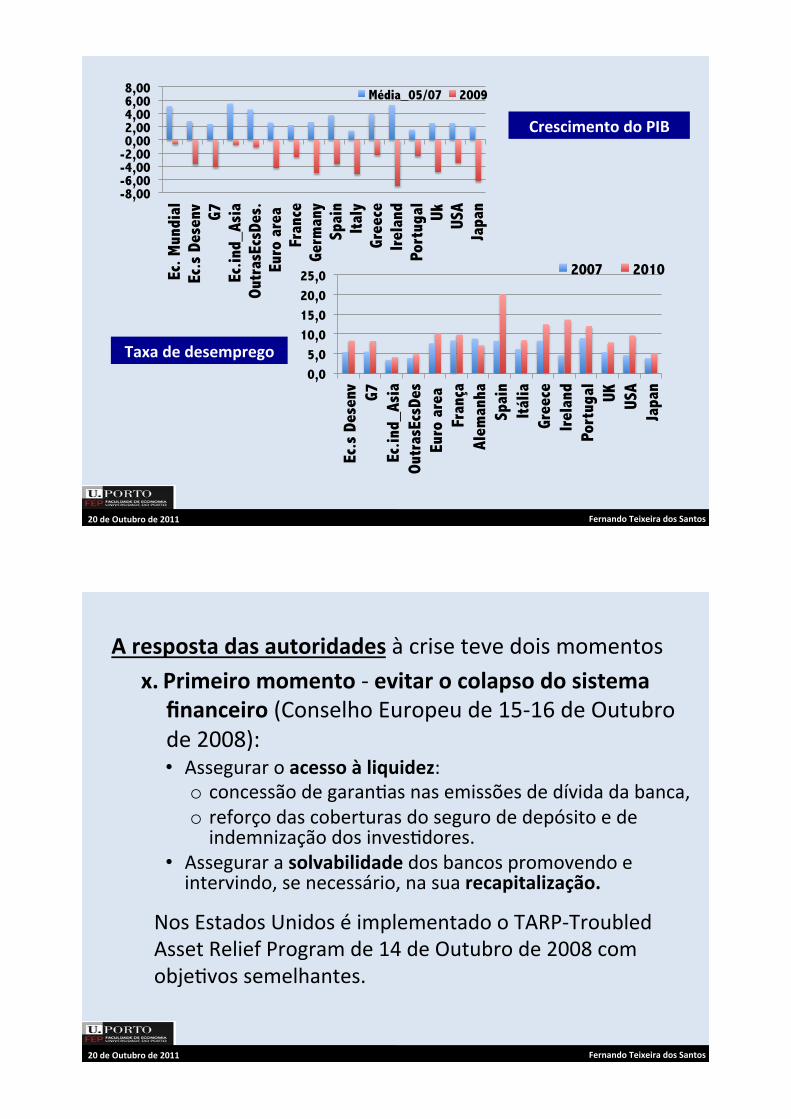

A#resposta#das#autoridades#à#crise#teve#dois#momentos#x. Primeiro#momento#[#evitar#o#colapso#do#sistema#

financeiro#(Conselho#Europeu#de#15[16#de#Outubro#de#2008):#• Assegurar#o#acesso#à#liquidez:##o concessão#de#garanEas#nas#emissões#de#dívida#da#banca,#o reforço#das#coberturas#do#seguro#de#depósito#e#de#indemnização#dos#invesEdores.##

• Assegurar#a#solvabilidade#dos#bancos#promovendo#e#intervindo,#se#necessário,#na#sua#recapitalização.#

#

Nos#Estados#Unidos#é#implementado#o#TARP[Troubled#Asset#Relief#Program#de#14#de#Outubro#de#2008#com#objeEvos#semelhantes.#

#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

#

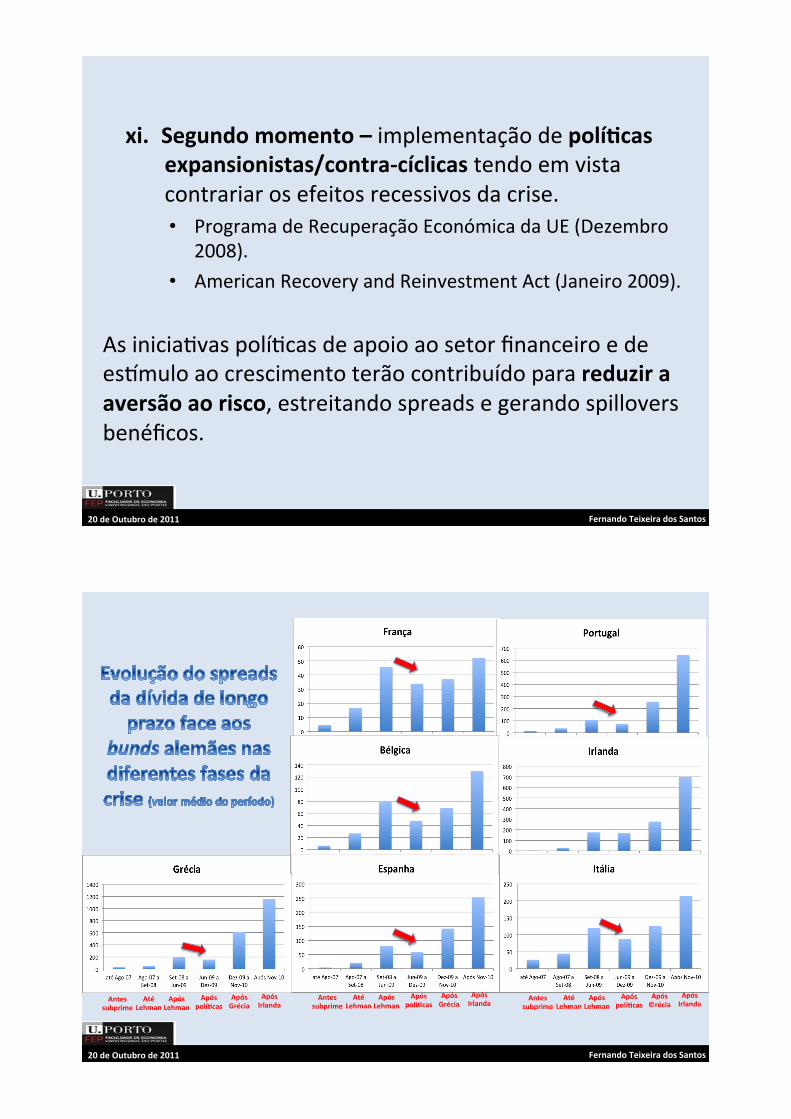

xi. Segundo#momento#–#implementação#de#políQcas#expansionistas/contra?cíclicas#tendo#em#vista#contrariar#os#efeitos#recessivos#da#crise.##• Programa#de#Recuperação#Económica#da#UE#(Dezembro#

2008).##• American#Recovery#and#Reinvestment#Act#(Janeiro#2009).##

As#iniciaEvas#políEcas#de#apoio#ao#setor#financeiro#e#de#estmulo#ao#crescimento#terão#contribuído#para#reduzir#a#aversão#ao#risco,#estreitando#spreads#e#gerando#spillovers#benéficos.#

##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Antes#subprime#

Até#Lehman#

Após#Lehman#

Após#políQcas#

Após#Grécia#

Após#Irlanda#

Antes#subprime#

Até#Lehman#

Após#Lehman#

Após#políQcas#

Após#©récia#

Após#Irlanda#

Antes#subprime#

Até#Lehman#

Após#Lehman#

Após#políQcas#

Após#Grécia#

Após#Irlanda#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

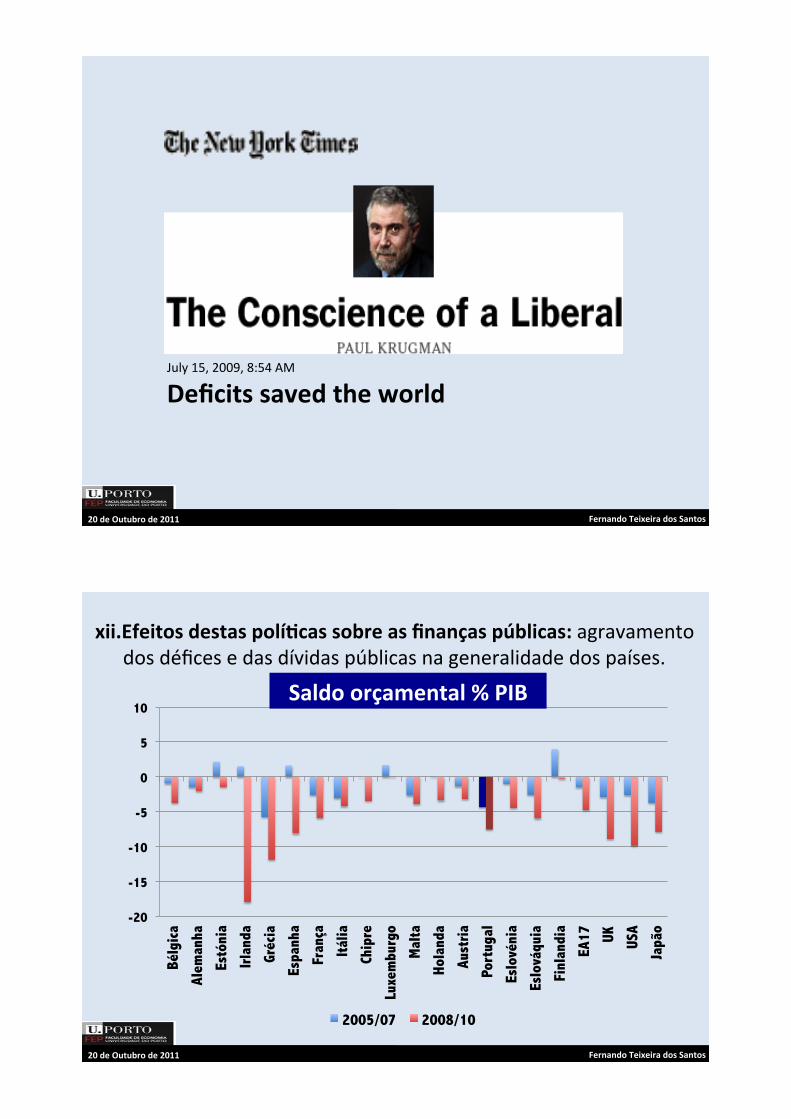

July#15,#2009,#8:54#AM#

Deficits#saved#the#world#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

xii. Efeitos#destas#políQcas#sobre#as#finanças#públicas:#agravamento#dos#défices#e#das#dívidas#públicas#na#generalidade#dos#países.##

-20

-15

-10

-5

0

5

10

Bélg

ica

Alem

anha

Estó

nia

Irla

nda

Gréc

ia

Espa

nha

Fran

ça

Itál

ia

Chip

re

Luxe

mbu

rgo

Mal

ta

Hola

nda

Aust

ria

Port

ugal

Eslo

véni

a

Eslo

váqu

ia

Finl

andi

a

EA17

UK

USA

Japã

o

2005/07 2008/10

Saldo#orçamental#%#PIB#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

0

50

100

150

200

250

Bélg

ica

Alem

anha

Es

tóni

a Ir

land

a Gr

écia

Es

panh

a Fr

ança

It

ália

Ch

ipre

Lu

xem

burg

o M

alta

Ho

land

a Au

stri

a Po

rtug

al

Eslo

véni

a Es

lová

quia

Fi

nlan

dia

EA17

UK

US

A Ja

pão

2005/07 2008/10

Dívida#pública#%#PIB#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

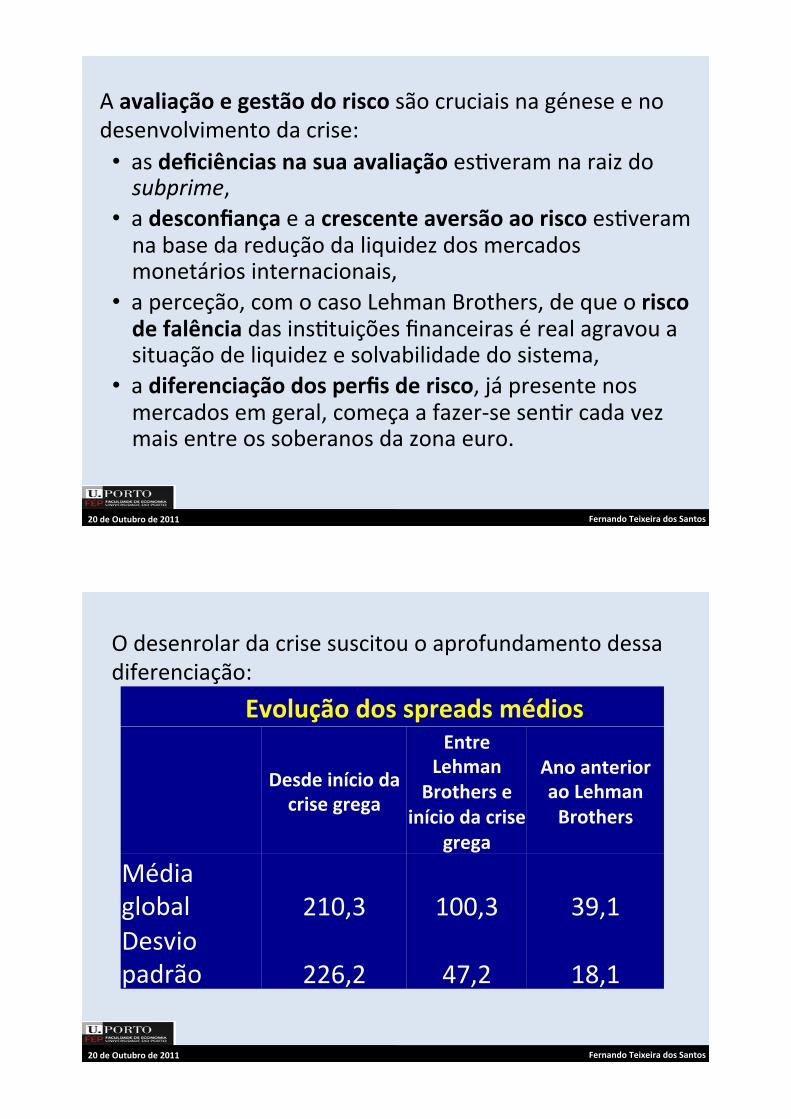

A#avaliação#e#gestão#do#risco#são#cruciais#na#génese#e#no#desenvolvimento#da#crise:#• as#deficiências#na#sua#avaliação#esEveram#na#raiz#do#subprime,##

• a#desconfiança#e#a#crescente#aversão#ao#risco#esEveram#na#base#da#redução#da#liquidez#dos#mercados#monetários#internacionais,##

• a#perceção,#com#o#caso#Lehman#Brothers,#de#que#o#risco#de#falência#das#insEtuições#financeiras#é#real#agravou#a#situação#de#liquidez#e#solvabilidade#do#sistema,#

• a#diferenciação#dos#perfis#de#risco,#já#presente#nos#mercados#em#geral,#começa#a#fazer[se#senEr#cada#vez#mais#entre#os#soberanos#da#zona#euro.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

O#desenrolar#da#crise#suscitou#o#aprofundamento#dessa#diferenciação:#

Desde#início#da##crise#grega##

Entre#Lehman#

Brothers#e#início#da#crise#

grega#

Ano#anterior#ao#Lehman#Brothers#

Média#global# 210,3# 100,3# 39,1#Desvio#padrão# 226,2# 47,2# 18,1#

#######Evolução#dos#spreads#médios##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

• O#agravamento#da#situação#das#finanças#públicas,#• Os#desafios#colocados#à#sua#sustentabilidade#pelo#envelhecimento#da#população#(aumento#da#esperança#de#vida#na#UE#em#cerca#de#7#a#8#anos#no#próximo#meio#século),#

• A#redução#significaEva#do#potencial#de#crescimento#nas#próximas#décadas,#agravada#pelos#efeitos#da#crise#(crescimento#anual#potencial#na#UE#de#2,4%#até#2020,#1,7%#entre#2020#e#2040#e#1,3%#após#2040)#e#

• Os#desequilíbrios#externos#significaEvos#em#vários#países,nalguns#casos#associados#a#elevados#níveis#de#endividamento,#

#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

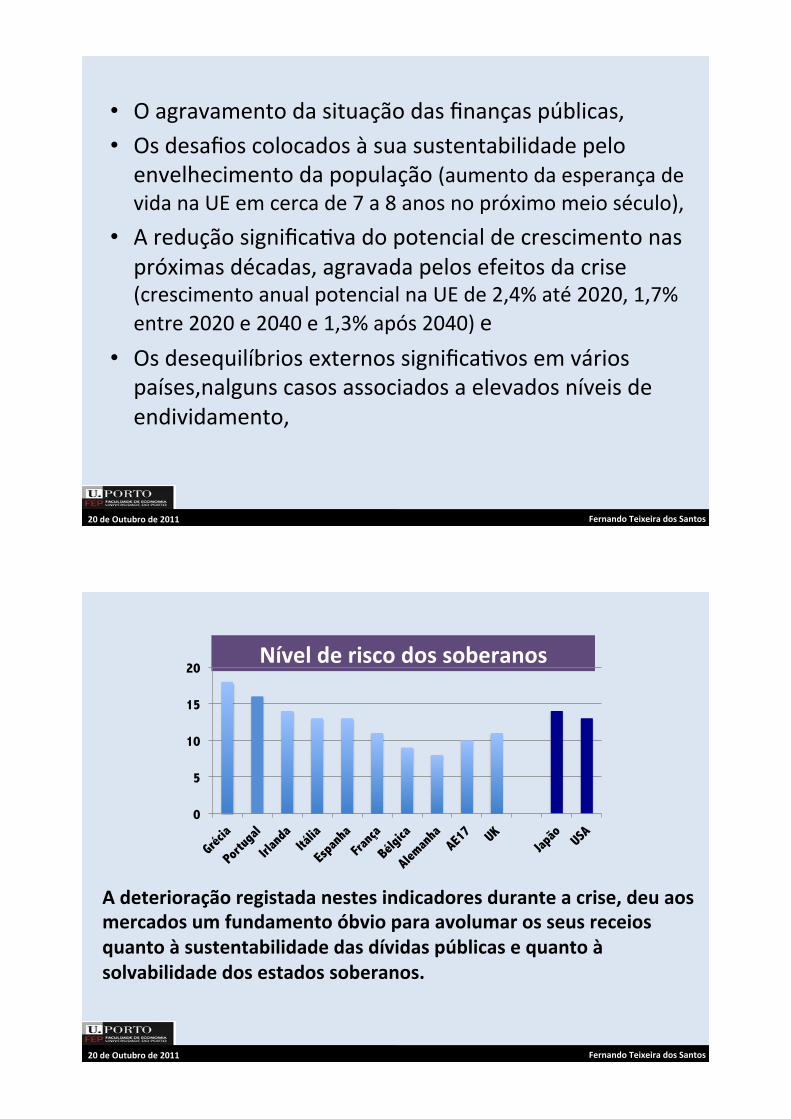

Nível#de#risco#dos#soberanos#

0

5

10

15

20

A#deterioração#registada#nestes#indicadores#durante#a#crise,#deu#aos#mercados#um#fundamento#óbvio#para#avolumar#os#seus#receios#quanto#à#sustentabilidade#das#dívidas#públicas#e#quanto#à#solvabilidade#dos#estados#soberanos.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

À#medida#que#a#perceção#de#risco#de#incumprimento#(default)#dos#estados#mais#endividados#se#foi#avolumando#nos#mercados#financiadores,##a#crise#foi#passando#do#sector#financeiro#para#os#estados#soberanos.##

O#caso#grego,#pela#sua#dimensão#e#pela#sua#falta#de#transparência,#reforçou#o#receio#de#insolvência#dos#soberanos,#foi#assim#um#catalizador#da#crise#contagiando#outras#economias#da#Zona#Euro.###

O#caso#grego#é#o#Lehman#Brothers#da#crise#da#dívida#soberana.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

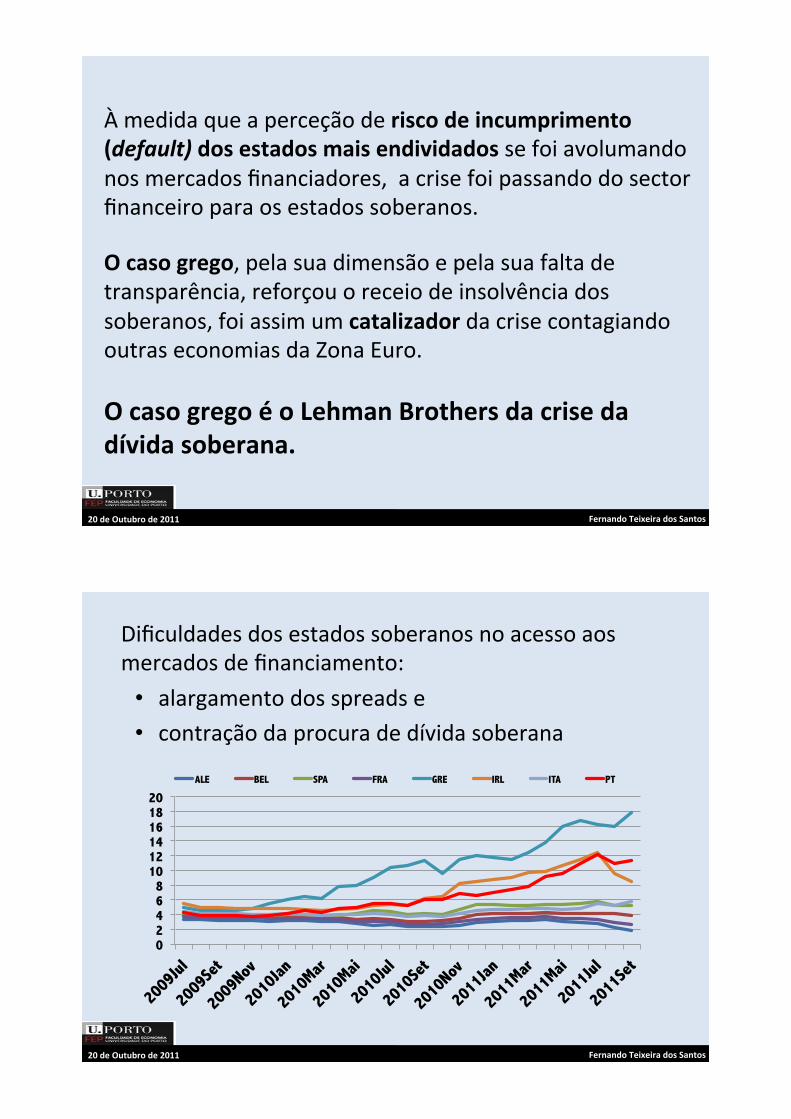

Dificuldades#dos#estados#soberanos#no#acesso#aos#mercados#de#financiamento:#• alargamento#dos#spreads#e##• contração#da#procura#de#dívida#soberana#

0 2 4 6 8

10 12 14 16 18 20

ALE BEL SPA FRA GRE IRL ITA PT

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

O#recurso#a#meios#alternaEvos#de#financiamento,#através#da#celebração#de#programas#de#assistência#externa#tornou[se#assim#inevitável#para#evitar#situações#de#insolvência.##

Foi#o#caso#da#Grécia#em#Maio#de#2010,#da#Irlanda#em#Novembro#desse#ano#e#de#Portugal#em#Abril#passado.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

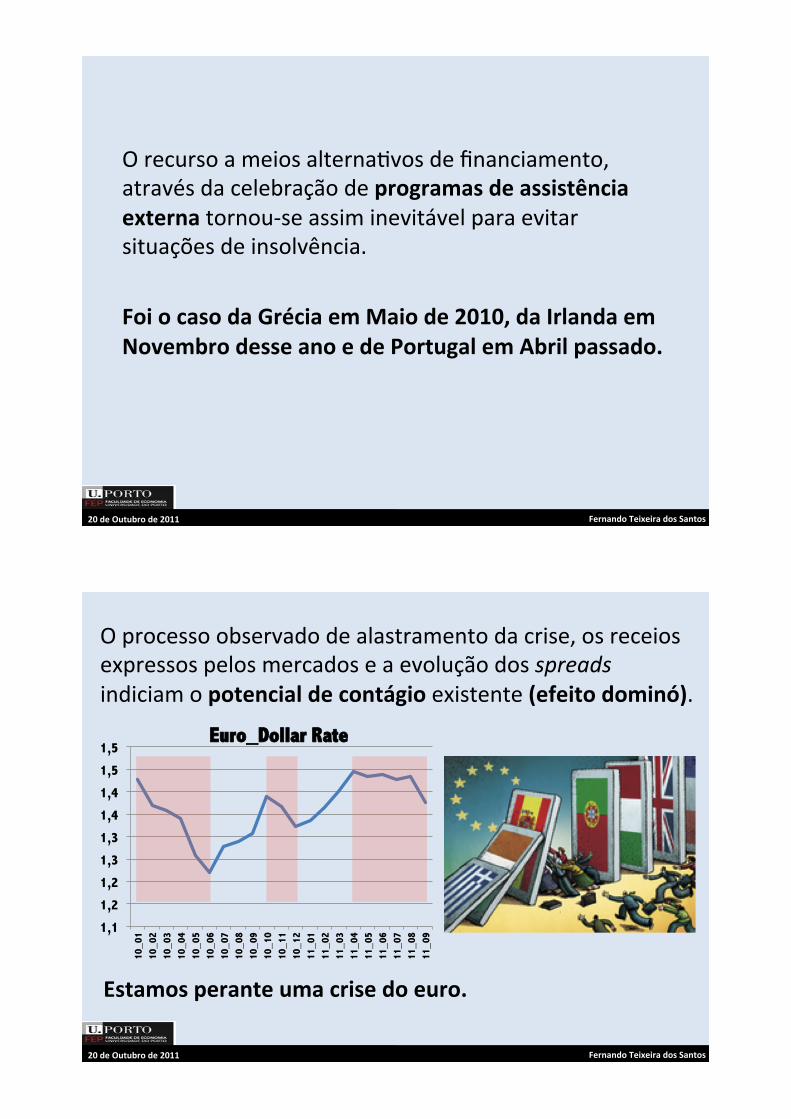

O#processo#observado#de#alastramento#da#crise,#os#receios#expressos#pelos#mercados#e#a#evolução#dos#spreads#indiciam#o#potencial#de#contágio#existente#(efeito#dominó).##

Estamos#perante#uma#crise#do#euro.#

1,1

1,2

1,2

1,3

1,3

1,4

1,4

1,5

1,5

10_0

1 10

_02

10_0

3 10

_04

10_0

5 10

_06

10_0

7 10

_08

10_0

9 10

_10

10_1

1 10

_12

11_0

1 11

_02

11_0

3 11

_04

11_0

5 11

_06

11_0

7 11

_08

11_0

9

Euro_Dollar Rate

#####

#####

#####

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Os#troubled-assets-do#subprime)#geraram#sérios#problemas#de#liquidez#e#puseram#em#causa#a#solvabilidade#dos#bancos.#Atualmente,#o#aEvo#tóxico#é#a#dívida#dos#troubled-sovereigns)que#se#encontra#nos#seus#balanços.#

Soberanos# Bancos# Economia#

Dificuldades#de#liquidez#

Risco#e/ou#insolvência#

Restrição#de#liquidez#nos#bancos#

Risco#e/ou#eventos#de#default#

Credit#crunch#

Efeitos#económicos#recessivos#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

!

!!!

Ms. Lagarde's recapitalization plan makes sense

Globe and Mail Blog Posted on Monday, August 29, 2011 4:30PM EDT !

October 13, 2011

Economics and Strategy Country Scoring in a Monetary Union

The financial crisis and subsequent economic fallout have exposed the eurozone’s deep heterogeneity. With country factors now becoming much more important for investment decisions, we have built an economic fundamental ranking model to compare and contrast eurozone countries across a number of dimensions.

We have crunched hundreds of indicators With eurozone sovereigns now behaving more like credit rather than government debt, country risk analysis is back in vogue. Over the past several weeks we have received an increasing number of requests from investors for key risk indicators for all eurozone economies. In this report we address these questions.

and built a risk ranking for the eurozone Based on the dataset that we assembled, we have constructed a subjective Euro Macro-Financial Ranking (E-MFR) model, which compares eurozone countries based on a broad set of economic, fiscal, financial and institutional variables capturing different macro and micro aspects.

that goes beyond the fiscal picture: Public debts and deficits are obvious starting points, but exclusively focusing on these indicators is too a narrow and short-term ‘old school’ approach, in our view. Eurozone countries’ long-term growth potential, which depends on their structural features, matters a great deal.

What our ranking tool says: Rather than a clear-cut core/periphery divide, there is a continuum ranging from strong-core to weak-peripherals. France is the ‘typical’ eurozone country, while Belgium looks stronger than assumed. Italy and Spain are burdened by public and private debts respectively, and have the same ranking. Ireland outperforms in terms of structural features.

From strong-core to weak-peripherals Euro Macro-Financial Ranking

0 2 4 6 8 10

FinlandGermany

AustriaBelgium

NetherlandsFranceIreland

ItalySpain

PortugalGreece

weaker

stronger

Source: Morgan Stanley Research

Key interest rate strategy views (L. Mutkin, E. Lin) - 5s30s French flattener vs. German steepener in cash; sell 5y French CDS Basis - 3s10s Belgium flattener vs. Germany

- 10s30s Italy flattener vs. Germany

- OW Spain vs. Italy - Favour Ireland vs. Portugal

- OW Germany, Belgium and Spain vs. UW Netherlands

- Germany: Long protection in CDS

Key equity strategy views (R. Carr) - Favour core over periphery

- Within the core, prefer exposure to the markets with lower macro risk and/or less cyclical exposure

- Prefer UK to eurozone – it ranks highly in MS country selection model, is less

cyclical than average and has been defensive in past recessions and bear markets

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. += Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M O R G A N S T A N L E Y R E S E A R C H E U R O P E

Morgan Stanley & Co. International plc+

Daniele Antonucci [email protected] +44 (0)20 7425 8943

Olivier Bizimana +44 (0)20 7425 6290

Elga Bartsch +44 (0)20 7425 5434

Tomasz Pietrzak

Anselm Karitter Laurence Mutkin, Elaine Lin, Ronan

Carr

0 5

10 15 20

Gréc

ia

Port

ugal

Ir

land

a It

ália

Es

panh

a Fr

ança

Bé

lgic

a Al

eman

ha

AE17

UK

Japã

o US

A

Christine Lagarde: Banks Need Urgent, Mandatory, Substantial Recapitalization Christine Lagarde|August 29, 2011|

• Note: This speech was published on the IMF website. Christine Lagarde delivered it at the Jackson Hole conference in 2011.

Merkel, Sarkozy Reach Deal On Bank Recapitalization

10/9/2011 11:11 PM ET

(RTTNews) - German Chancellor Angela Merkel and French President Nicolas Sarkozy have reached an agreement on recapitalizing European banks in an attempt to stem the debt crisis. They promised that the details of the plan will be announced by the end of this month.

!

Christine Lagarde: Banks Need Urgent, Mandatory, Substantial Recapitalization Christine Lagarde|August 29, 2011|

• Note: This speech was published on the IMF website. Christine Lagarde delivered it at the Jackson Hole conference in 2011.

Merkel, Sarkozy Reach Deal On Bank Recapitalization

10/9/2011 11:11 PM ET

(RTTNews) - German Chancellor Angela Merkel and French President Nicolas Sarkozy have reached an agreement on recapitalizing European banks in an attempt to stem the debt crisis. They promised that the details of the plan will be announced by the end of this month.

!

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Compete#às#autoridades#monetárias#definir,#coordenar##e#implementar#um#plano#adequado#de#recapitalizção#dos#bancos#.##

A#Reuters,#por#exemplo,#considera#haver#necessidade#de#injetar#cerca#de#93#mil#milhões#de#euros#em##47#bancos#europeus.##

C H A P T E R 1 OV E R CO M I N G P O L I T I C A L R I S K S A N D C R I S I S L E G AC I E S

balance sheet assets, liabilities, and income/losses on banks. A typical stress test would have several components that are beyond the scope of this exercise. For example, it would include an economic scenario that would result in rising losses on bank’s loan books, a marking to market of securities, including corporate bonds, and a projection of new income and how this would be a!ected by funding strains. In addition, it would include the size of capital bu!ers and provisions available to cushion increased losses, and from there it would derive a capital need.

"e epicenter of sovereign risk has been Greece, which generated the #rst of four waves of spillover to European banks. "e analysis suggests that, #rst, spillovers on European bank exposures to the Greek sovereign have amounted to almost $60 billion (Figure 1.17). Second, as sovereign risks spread to

other governments, the spillovers to banks have mounted. If the sovereign stresses in Ireland and Portugal are included, the total spillover rises to $80 billion. "ird, the governments in Belgium, Italy, and Spain have also come under market pressure; incorporating credit risks from these sovereigns into the analysis further raises the total estimated spillover, to about $200 billion. Fourth, bank asset prices in the high-spread euro area have fallen in concert with sovereign stresses, leading to a rise in the credit risk of interbank exposures; including those exposures increases the total estimated spillover to $300 billion overall. Although these numbers are based on market assessments of credit risk, which may re%ect a degree of overshooting, the underlying problems that they highlight are real.

Banking systems in the high-spread euro area are likely to be most a!ected.

"is aggregate picture masks a heterogeneous range of spillovers on country banking systems (Figure 1.18). High-spread euro area systems have faced the most severe spillovers from their local sovereigns. "e key exception to this is Cyprus, which has high spillovers from bank exposures to the Greek sovereign. A number of other banking systems�such as those of Luxembourg, France, and Germany�have experienced spillovers from the high-spread euro area to their foreign operations or cross-border exposures, but these represent a smaller percentage of assets. Finally, several European banking systems have had little or no spillover from high-spread euro area sovereigns.

Conducting the analysis on individual bank balance sheets con#rms the results of the aggregate

International Monetary Fund | September 2011 21

In sum, although losses are likely to have been recognized in the trading book, loss recognition has been slow and inconsistent in the banking book. To improve transparency, more clarity in the account-ing standards is required for the application of mark-to-market valuation for thinly traded govern-

ment bond markets and the method of provision-ing in HTM should be revisited. In addition, more consistency is needed in the recognition of AFS losses in regulatory capital across jurisdictions (see the discussion in the “Policy Priorities” section of the main text).

Box 1.3 (continued)

60 80 200 300

Spillovers from . . . Greek sovereignIrish and Portuguese sovereignsBelgian, Spanish, and Italian sovereignsHigh-spread euro area banking sector

Figure 1.17. Cumulative Spillovers from High-Spread Euro Area Sovereigns to the European Union Banking System(Billions of euros)

Source: IMF sta" estimates.Note: The size of the circles is proportional to the size of the spillover.

Includes banking systems in 20 European Union countries. The high-spread euro area countries are Belgium, Greece, Ireland, Italy, Portugal, and Spain. Figures are rounded to the nearest 10 billion euros.

C H A P T E R 1 OV E R CO M I N G P O L I T I C A L R I S K S A N D C R I S I S L E G AC I E S

balance sheet assets, liabilities, and income/losses on banks. A typical stress test would have several components that are beyond the scope of this exercise. For example, it would include an economic scenario that would result in rising losses on bank’s loan books, a marking to market of securities, including corporate bonds, and a projection of new income and how this would be a!ected by funding strains. In addition, it would include the size of capital bu!ers and provisions available to cushion increased losses, and from there it would derive a capital need.

"e epicenter of sovereign risk has been Greece, which generated the #rst of four waves of spillover to European banks. "e analysis suggests that, #rst, spillovers on European bank exposures to the Greek sovereign have amounted to almost $60 billion (Figure 1.17). Second, as sovereign risks spread to

other governments, the spillovers to banks have mounted. If the sovereign stresses in Ireland and Portugal are included, the total spillover rises to $80 billion. "ird, the governments in Belgium, Italy, and Spain have also come under market pressure; incorporating credit risks from these sovereigns into the analysis further raises the total estimated spillover, to about $200 billion. Fourth, bank asset prices in the high-spread euro area have fallen in concert with sovereign stresses, leading to a rise in the credit risk of interbank exposures; including those exposures increases the total estimated spillover to $300 billion overall. Although these numbers are based on market assessments of credit risk, which may re%ect a degree of overshooting, the underlying problems that they highlight are real.

Banking systems in the high-spread euro area are likely to be most a!ected.

"is aggregate picture masks a heterogeneous range of spillovers on country banking systems (Figure 1.18). High-spread euro area systems have faced the most severe spillovers from their local sovereigns. "e key exception to this is Cyprus, which has high spillovers from bank exposures to the Greek sovereign. A number of other banking systems�such as those of Luxembourg, France, and Germany�have experienced spillovers from the high-spread euro area to their foreign operations or cross-border exposures, but these represent a smaller percentage of assets. Finally, several European banking systems have had little or no spillover from high-spread euro area sovereigns.

Conducting the analysis on individual bank balance sheets con#rms the results of the aggregate

International Monetary Fund | September 2011 21

In sum, although losses are likely to have been recognized in the trading book, loss recognition has been slow and inconsistent in the banking book. To improve transparency, more clarity in the account-ing standards is required for the application of mark-to-market valuation for thinly traded govern-

ment bond markets and the method of provision-ing in HTM should be revisited. In addition, more consistency is needed in the recognition of AFS losses in regulatory capital across jurisdictions (see the discussion in the “Policy Priorities” section of the main text).

Box 1.3 (continued)

60 80 200 300

Spillovers from . . . Greek sovereignIrish and Portuguese sovereignsBelgian, Spanish, and Italian sovereignsHigh-spread euro area banking sector

Figure 1.17. Cumulative Spillovers from High-Spread Euro Area Sovereigns to the European Union Banking System(Billions of euros)

Source: IMF sta" estimates.Note: The size of the circles is proportional to the size of the spillover.

Includes banking systems in 20 European Union countries. The high-spread euro area countries are Belgium, Greece, Ireland, Italy, Portugal, and Spain. Figures are rounded to the nearest 10 billion euros.

O#FMI#avalia#o#impacto#dos#efeitos#de#spillover#entre#os#200#e#300#mil#milhões.##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

A#crise#que#atualmente#vivemos#reflete[se#em:#

• Problemas#de#liquidez#e#risco#de#insolvência#de#soberanos,#

• Problemas#de#liquidez#no#sistema#de#crédito,#

• Risco#de#insolvência#de#insEtuições#bancárias#provocado#por#eventuais#eventos#de#default)soberano,#

• Efeitos#recessivos#sobre#a#economia#resultantes##[ das#políEcas#restrivas#de#ajustamento#[ da#falta#de#financiamento#[ do#estado#negaEvo#das#expectaEvas##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

#

A#hesitação#dos#responsáveis#europeus#na#adoção#de#medidas#capazes#de#superar#a#crise#é#geradora#de#incerteza#adicional#e#tem#sido#por#isso,#mais#um#fator#de#agravamento#da#crise.##Perante#o#cenário#cada#vez#mais#provável#de#reestruturação#da#dívida#grega,#as#autoridades#europeias#não#têm#contribuído#para#a#clarificação#rápida#da#situação,#o#que#só#tem#agravado#as#suas#consequências#sobre#o#setor#financeiro.##Tal#tem#afetado#os#bancos#mais#expostos#à#dívida#soberana#dos#troubled)sovereigns,#contagiando#assim#os#países#de#origem#desses#bancos.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

A#crise#tem#revelado#sérias#deficiências#do#quadro#insQtucional#e#políQco#em#que#assenta#a#moeda#única.#Tornou[se#claro#que#o#modelo#de##• uma#políEca#monetária#única/comum#e#• várias#políEcas#orçamentais#nacionais#

não#foi#capaz#de#conferir#à#Zona#Euro#o#pilar#orçamental#indispensável#para#prevenir#e#responder#a#crises#como#aquela#que#nos#tem#afetado.###Por#isso,#a#saída#da#crise#requer#uma#resposta#a#dois#niveis:#

##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

A#nível#nacional:##• Assegurar#a#estabilidade#e#a#solvabilidade#dos#seus#sistemas#financeiros#

• #Colocar#os#défices#e#as#dívidas#em#trajetórias#de#correção#credíveis#e#sustentáveis#de#modo#a#aEngirem#o#mais#rapidamente#possível#os#seus#objeEvos#de#médio#prazo,##

• Adotar#as#reformas#indispensáveis#para#promover#a#sustentabilidade#e#maior#qualidade#das#finanças#públicas,#

• Incorporar#nos#quadros#orçamentais#nacionais#os#objeEvos#e#princípios#comunitários#de#governação#da#políEca#orçamental,#

• Implementar#reformas#que#reforcem#o#crescimento#potencial#e#a#compeEEvidade#das#suas#economias.###

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

ii. A#nível#europeu,#é#necessário:#• Reforçar#a#coordenação#das#políEcas#económicas#e#a#governação#do#euro:##o recomendações#mais#vinculaEvas,##o sanções#efeEvas#e#céleres#que#previnam#e#corrijam#

comportamentos#desviantes#dos#estados#membros,#

• Reforçar#os#mecanismos#de#prevenção#e#resolução#de#crises,###

• Reforçar#os#poderes#de#decisão#e#intervenção#das#autoridades#comunitárias#(COM#e#Conselho)#na#definição,#execução,#acompanhamento#e#vigilância#das#políEcas#económicas,#

• Sistema#europeu#reforçado#de#supervisão#financeira.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Estes#dois#níveis#devem#estar#deviadamente#coordenados#e#balanceados.#O#enfoque,#como#tem#ocorrido#até#ao#momento,#no#esforço#nacional#é#insuficiente#e#ineficiente.#

#

Mas#a#resposta#europeia#não#se#esgota#nas#iniciaEvas#acabadas#de#referir.#A#sua#concreEzação#exige#um#processo#políEco#e#tempo#que#não#se#compadecem#com#a#necessidade#de#resposta#urgente#que#o#estado#atual#da#crise#exige.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Estancar#e#resolver#a#crise#que#grassa#exige,#a#nível#europeu:#a) Esclarecer,#quanto#antes,#que#países#são#considerados#insolventes,#em#parEcular#o#caso#da#Grécia.##

b) #Resolver#a#situação#dos#países#insolventes,#mantendo[os#no#euro,#promovendo#as#operações#necessárias,#eventualmente##a#reestruturação#da#sua#dívida#e#o#envolvimento#dos#credores#privados.#

c) Implementar#medidas#que#evitem#efeitos#de#spillover#sobre#os#países#solventes.#Dever[se[á,#designadamente,#avaliar#o#impacto#no#sistema#bancário#exposto#às#dívidas#soberanas#em#questão#e#providenciar#a#sua#solidez#financeira.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

d) Assegurar#que#os#países#solventes#terão#acesso#aos#meios#de#financiamento#necessários.##

Idem#para#o#sistema#bancário.#

e) Evitar#fenómenos#de#moral-hazard.#Deve#ser#manEdo#um#quadro#de#estrita#condicionalidade#e#os#países#envolvidos#deverão#ficar#sujeitos#a#regras#de#vigilância#e#avaliação#estritas.##

f) Implementação#de#uma#estratégia#coordenada#de#promoção#do#crescimento#por#parte#dos#estados#membros#com#“espaço#orçamental”#para#o#efeito.##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

O#sucesso#de#uma#iniciaEva#que#integre#este#Epo#de#elementos#depende##

• da#disponibilzação#dos#recursos#necessários#–#que#serão#avultados,#e##

• da#assunção#de#compromissos#políEcos#que#permitam#avançar#com#as#reformas#insEtucionais#atrás#referidas.#Apesar#de#operacionais#somente#a#médio#prazo,#são#relevantes#para#o#acordo#políEco#indispensável#no#imediato.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Perante#as#dúvidas#existentes#quanto#à#capacidade#da#Grécia#poder#cumprir#o#seu#programa,#Portugal#não#pode#falhar#no#cumprimento#do#seu#programa#de#ajustamento.#

#Precisamos#do#apoio#europeu,#e#a#Europa#precisa#da#nossa#disciplina#e#do#reforço#da#nossa#compeEEvidade#para#se#fortalecer#e#para#que#se#cumpra#o#desígnio#dos#fundadores#da#União#Europeia:##a#efeEva#convergência#entre#as#suas#economias.##

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

A#resolução#da#crise#grega#não#deixará#de#ter#implicações#para#Portugal.##

Apesar#das#medidas#que#possam#ser#adotadas#para#evitar#fenómenos#de#contágio,#é#de#esperar#que#haja#mais#condicionalidade#e#que#tenhamos#que#parQlhar#mais#decisões#com#os#nossos#parceiros#e#insEtuições#comunitárias,#nas#quais#temos#sido#soberanos#até#agora.##

Mas#estando#em#causa#a#recuperação#da#confiança#dos#mercados#em#Portugal,#a#dimensão#do#esforço#em#curso#e#o#quadro#de#rigor,#disciplina#e#condicionalidade#no#qual#ele#se#desenvolve#são#elementos#credibilizadores#importantes.#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

Temos#que#ter#consciência#que#o#ajustamento#a#efetuar#é#grande#e#que#exige#sacri}cios#muito#significaEvos.#Sacriucios#incontornáveis#e#inadiáveis.##Mas#sacri}cios##• que#devem#ser#exigidos#com#senQdo#de#equidade#e#de#proporcionalidade#e##

• que#não#podem#ignorar#as#exigências#de#relançamento,#a#prazo,#de#um#forte#crescimento#económico.#

##

#

20#de#Outubro#de#2011#Fernando#Teixeira#dos#Santos#20#de#Outubro#de#2011#

FIM#